Content

What is the Sludge Treatment Chemicals Market Size and Share?

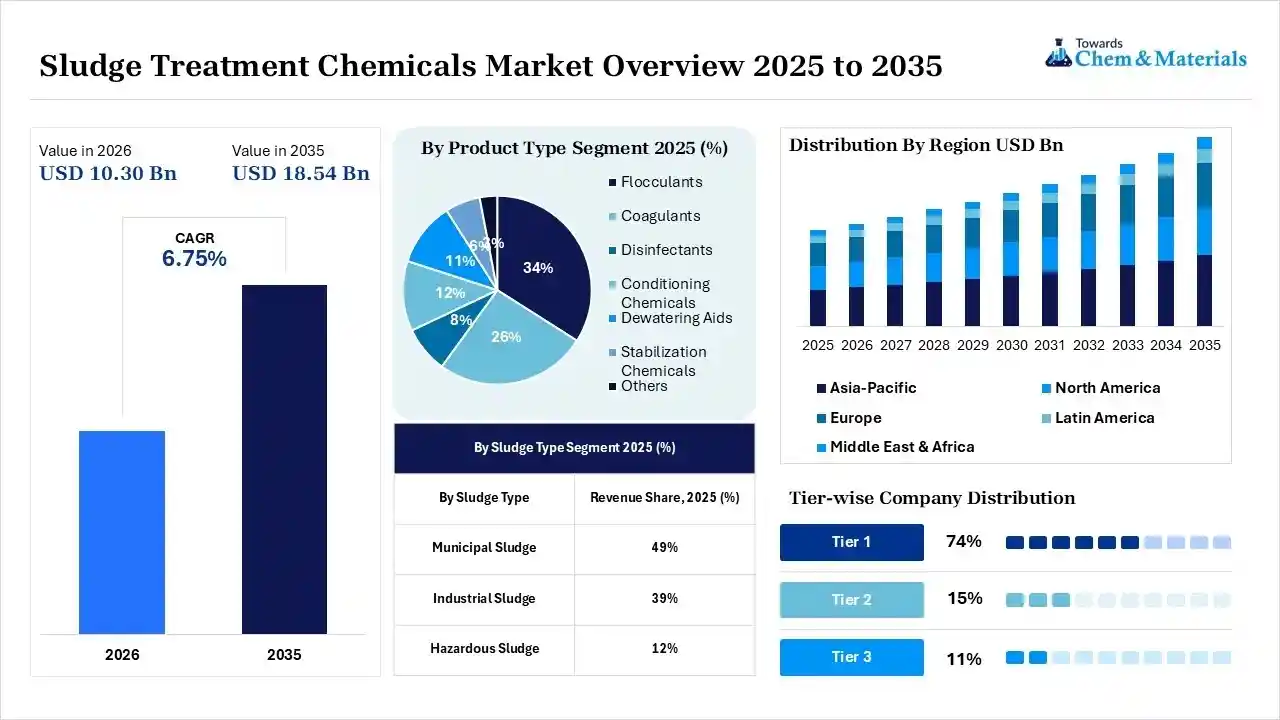

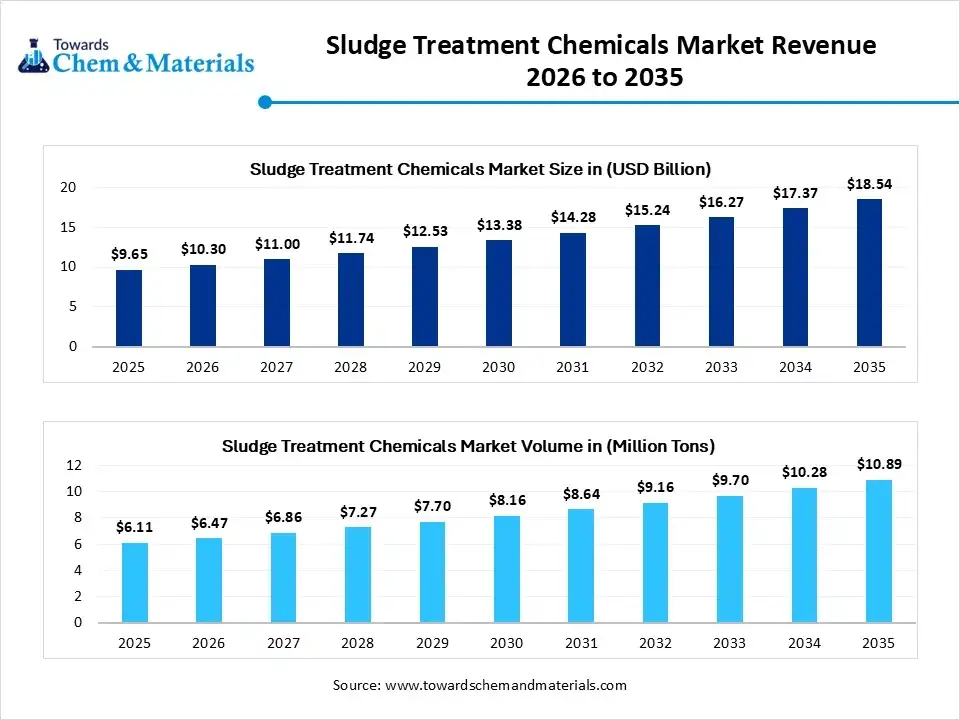

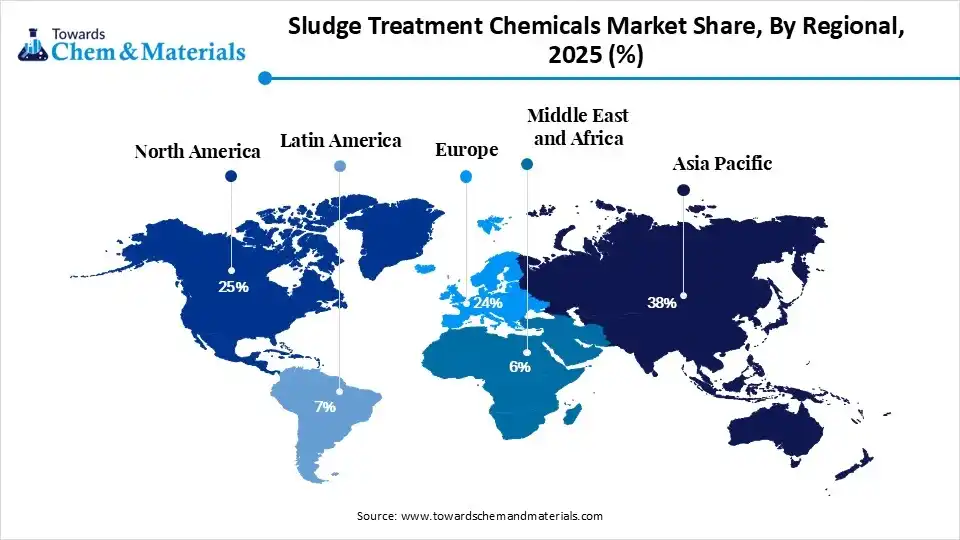

The sludge treatment chemicals market size was valued at USD 9.65 billion in 2025, is estimated to reach USD 10.30 billion in 2026, and is projected to reach USD 18.54 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.75% over the forecast period from 2026 to 2035.Asia Pacific dominated the sludge treatment chemicals market with the largest revenue share of 38% in 2025 and is expected to grow at the fastest CAGR of 6.88% during the forecast period. In terms of volume, the sludge treatment chemicals market is projected to grow from 6.11 million tons in 2025 to 10.89 million tons by 2035. growing at a CAGR of 5.95% from 2026 to 2035.The market growth is supported by technological advancements for waste treatment, stringent environmental standards, and investment in treatment infrastructure. These sludges are categorized into municipal and industrial sludges, promoted by substance investment and resource recovery projects.

Market Highlights

- By region, Asia Pacific dominated the sludge treatment chemicals market by holding a 38% share in 2025 due to municipal wastewater infrastructure and regulatory compliance.

- By region, North America held the 25% market share in 2025 and is expected to grow at the fastest with a CAGR of 7.60% during the forecast period, driven by domestic demand for advanced treatment and environmental standards.

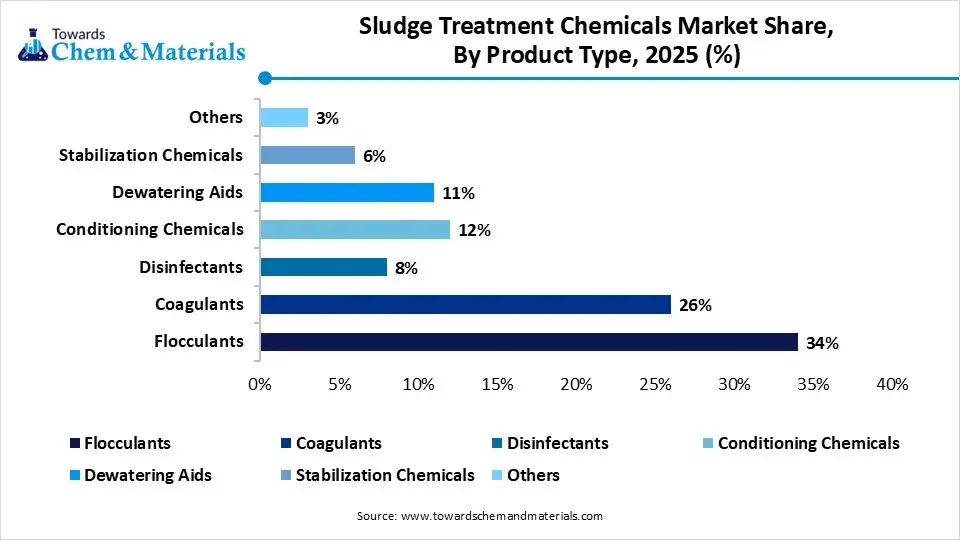

- By product type, the flocculants segment dominated the market with the largest share of 34% in 2025, accelerated by demand in sludge solid-liquid separation and municipal treatment facilities.

- By product type, the dewatering aids segment held 11% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period, driven by technological advancement and rising disposal costs.

- By sludge type, the municipal sludge segment dominated the market with the largest share of 49% in 2025, driven by rapid urbanization and investment for treatment expansion.

- By sludge type, the industrial sludge segment held 39% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period due to stringent discharge regulations and slug volume in manufacturing expansion.

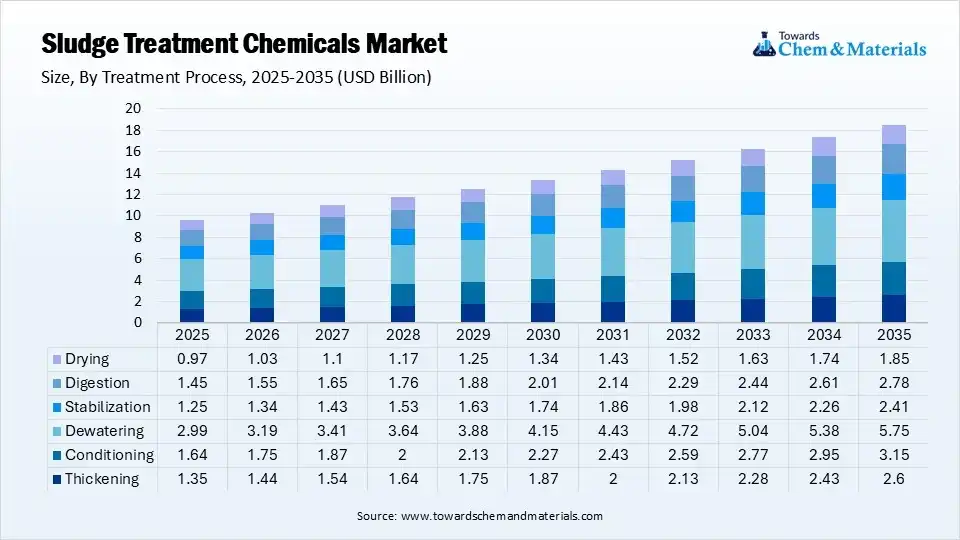

- By treatment process, the dewatering segment dominated the market with the largest share of 31% in 2025, driven by advanced dewatering technologies and rising sludge disposal costs.

- By treatment process, the digestion segment held 15% market share in 2025 and is expected to grow at the fastest CAGR of 7.30% over the forecast period due to expansion in resource recovery projects and biogas generation initiatives.

- By application, the municipal wastewater treatment segment dominated the market with the largest share of 46% in 2025, boosted by wastewater treatment infrastructure investment supported by the expanding urban population.

- By application, the industrial wastewater treatment segment held 31% market share in 2025 and is expected to grow at the fastest CAGR of 7.2% over the forecast period due to manufacturing expansion and industrial compliance.

- By end-use industry, the municipal utilities segment dominated the market with the largest share of 42% in 2025 due to large-scale wastewater treatment operations and government support.

- By end-use industry, the chemicals & petrochemicals segment held 12% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period, driven by complex wastewater stream advancement and high-volume chemical demand.

Quick At a Glance

- Market in Size (2025): USD 9.65 Billion | CAGR (2026–2035): 6.75%

- Market Estimated size in 2026: USD 10.30 Billion

- Market Projected Size (2035): USD 18.54 Billion

- Asia Pacific: largest Regional Market Revenue Share of 38% in 2025| USD 3.67 Billion

- North America: Fastest-growing Regional Market Revenue Share of 25% in 2025| USD 2.41 Billion

- By country: The China held the largest market share of 39.0% in 2025

- Market in Volume (2025): 6.11 Million Tons| Volume CAGR (2026–2035): 5.95%

- Market Estimated Volume (2026): 6.47 Million Tons

- Market Projected Volume (2035): 10.89 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 1,120/Ton

- Average Selling Price: USD 1,560/Ton

- Pricing CAGR (2026–2035): 2.60%

Market Overview

The sludge treatment chemicals market is shifting from basic disposal to advanced resource recovery. The expansion is driven by stringent regulations and rising waste volumes from the urban population. The current innovation focuses on green chemistry and bio-based polymers as establishments improve ESG scores. Many government-supported projects focus on enhancing and applying sludge dewatering solutions to accelerate domestic growth.

- In January 2026, SUEZ secured an agreement to supply a sludge dewatering solution for Hong Kong's largest sewage treatment plant in Caverns. This project comprises relocating the Sha Tin Sewage Treatment Works to the Caverns site, directed by the Drainage Services Department (DSD) of the Hong Kong SAR Government, setting a new standard in Asia.(Source: www.prnewswire.com)

Wastewater plants use anaerobic digestion to convert organic waste into renewable energy, producing biogas and heat, allowing long-term growth through modern, sustainable infrastructure. Coagulants and flocculants are vital for solid-liquid separation, improving dewatering by lowering sludge volume and reducing costs by promoting logistics and disposal by preparing sludge for additional treatment. The sludge treatment chemicals market is implementing phosphorus recovery technology that utilizes chemical precipitants to extract nutrients from sludge, thereby avoiding eutrophication and creating fertilizer feedstock. The consumer and industrial demand for biodegradable alternatives derived from natural sources, such as starch and tannins, offering low toxicity and high performance in solid-liquid separation.

Rapid urbanization enables municipal wastewater facilities to integrate automated dosing with real-time sensors, thereby reducing waste and optimizing effluent chemical oxygen demand to achieve economic viability. The emerging opportunity relies on customizing chemical treatments to handle complex industrial sludge from pharmaceuticals and textiles, which generate heavy-metal waste and dyes that require advanced stabilization. Major players' strategic partnerships are shifting toward service-oriented, site-specific formulations of treatment chemicals to meet safety standards. Sludge treatment chemicals, combining advanced chemistry with digital monitoring, are crucial for water reclamation and maintaining the hydrological cycle. Overall, the sludge treatment chemicals function as resilient infrastructure, fostering industrial growth and protecting eco-friendly ecosystems.

Growing Urbanization Fuels Demand for Sludge Treatment Chemicals

The rapid growth in urbanization in many countries increases the sludge water production. Factors like growing populations in some countries, rapid growth in industrialization, and increased wastewater volume increase demand for effective chemicals for sludge treatment. The growing urban areas generate more wastewater, and a high volume of wastewater consists of more sludge, which requires effective treatment.

The increasing population in many urban areas is leading to more generation of wastewater and sludge. The growing urbanization increases demand for advanced treatment methods to comply with stringent regulations and address environmental problems. The growing expansion of cities increases demand for chemicals like disinfectants, coagulants, and flocculants for effective sludge treatment. Urbanization helps in the growth of industrialization, which increases wastewater generation. Industrialization is responsible for increased sludge volume, which increases demand for effective treatments. The growing urbanization is a key driver for the sludge treatment chemicals market growth.

")

Global Investment Flow for the Sludge Treatment Chemicals Market

The investment infrastructure in the sludge treatment chemicals market moves towards resource harvesting, with capital venture into chemical solutions for nutrient mining from municipal waste streams.

- In June 2025, Solenis and NCH Corporation announced their agreement to merge, with Solenis set to acquire 100% of NCH's stock. This blend will create a more expanded, customer-focused provider of water and hygiene solutions.(Source: www.nch.com)

The government funding and green energy mandates align with automation firms that promote plant-driven coagulants and biosolid stabilization due to water insufficiency and local fertilizer requirements.

This capital surge is for strategic collaboration and acquisition of low-toxicity treatment agents. Overall, investments are shifting toward well-established technologies that convert environmental costs into profitable and renewable energy sources.

Market Trends

- Move Towards Nutrient Harvesting Hubs: Modern sludge treatment facilities utilizing specialized precipitants for mineral extraction. This hub focuses on transforming hazardous sludge into valuable fertilizer feedstocks.

- Upsurge of Plant-Originated Chemical Solutions: To meet corporate green mandates, pushing manufacturers toward the adoption of renewable coagulant formulations such as starch and tannins, influenced by biodegradability and non-toxicity.

- Catalysing Energy Self-Sufficiency: Innovative treatment process utilises organic solids and anaerobic bacteria for chemical breakdown, simplifying the sludge for renewable power generation.

Market Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 10.30 Billion / 6.47 Million Tons |

| Revenue Forecast in 2035 | USD 18.54 Billion / 10.89 Million Tons |

| Growth Rate | CAGR 6.75% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Product Type, By Sludge Type, By Treatment Process, By Application, By End-Use Industry, By Regions |

| Key Companies Profiled | Kemira Oyj, BASF SE, AkzoNobel, Ashland, Shandong, DowDuPont, Ecolab Inc., Lonza, Suez S.A., Kurita Water Industries Ltd., Buckman Laboratories International Inc., Feralco Group, ChemTreat, Inc., Solenis LLC, Accepta Ltd., Thermax Limited, Veolia Water Technologies & Solutions |

Key Technological Shifts and AI in the Sludge Treatment Chemicals Market

The sludge treatment chemicals market is undergoing a digital transformation, making treatment processes more cost-effective, efficient, and eco-friendly through constant innovation. AI enhances the quality and quantity of municipal and industrial waste separation, reduces contamination, enhancing quality and boosts energy recovery.

Machine learning integrated with generative AI for the discovery of non-toxic and performance-driven sludge treatment chemicals. The IoT-based monitoring and automated sorting optimize real-time tracking, routing, and waste classification by leveraging wastewater treatment infrastructure investments.

Supply Chain Analysis of the Sludge Treatment Chemicals Market

- Feedstock Procurement & Synthesis of Chemical Precursors: The stage of sourcing green feedstock and synthesis of monomers, inorganic minerals, acrylamide, metallic salts, and organic residue by maintaining purity and lowering carbon footprint.

- DowDuPont: Known as a provider of high-purity intermediate monomers, it utilizes recycled plastic waste as a feedstock for wastewater polymers. The company focuses on a sustainable, high-performance starting point for the global supply chain.

- Key Players: BASF, Mitsubishi Chemical, ExxonMobil Chemical, and Huntsman Corporation.

- Polymerization and Formulation: This stage is where manufacturers transform raw chemicals into functional polymeric chains and conditioners. These chemical chains are incorporated into sludge types derived from oily refinery waste or municipal biosolids.

- SNF Group: The dominant manufacturers that specialize in the production of water-soluble polymers by offering ultra-high-molecular-weight flocculants that are precisely designed for high-speed centrifuges, ensuring the chemical longevity and performance for waste management.

- Major Players: Kemira, Kurita Water Industries, Nouryon Industry, and Solenis LLC

- System Integration and Precision Application: The final stage of Chemicals-as-a-Service, integrating adaptive dosing systems and digital monitoring tools to ensure precision. This stage is vital for operational efficiency, for agricultural reuse, septage treatment, landfill management, and energy conversion.

- Ecolab (Nalco Water): The company offer 3D TRASAR digital ecosystem. The Ecolab platform uses advanced sensors in the sludge stream to automatically adjust chemical injection during sludge treatment.

- Key Players: Veolia Water Technologies, Xylem, Univar Solutions, and Brenntag.

Regulatory Framework: Sludge Treatment Chemicals Market

| Region | Key Regulation | Regulatory Approach |

| Global | ISO Standards, UN Sustainable Development Goals | Standard for water security and sludge stabilization. Standards driving the implementation of low-toxicity chemical alternatives and energy recovery from waste streams. |

| Asia Pacific | China’s 14th Five-Year Action Plan & India's National Water Mission | Focus on modernizing municipal infrastructure and achieving zero liquid discharge, ensuring reduced sludge volumes and cleaner industrial effluents. |

| North America | EPA Clean Water Act and PFAS-Free Action Plan | The PFAS-free mandates and set limits for heavy metals, for advanced oxidation chemicals, and specialized stabilizers for diversified applications. |

| European Union | Urban Wastewater Treatment Directive and EU REACH Standards | Focus on nutrient recovery and banning of microplastics that enable the region to move towards biodegradable polymers and higher dewatering efficiency. |

Sludge Treatment Chemicals Market Dynamics

Driver

Rising Global Regulatory Mandates for Industrial Waste Neutralization

The sludge treatment chemicals industry is driven by stringent discharge protocols and legally binding standards for public and private chemical operators. The environmental company uses advanced monitoring to prevent hazardous chemical residues from leaching into sustainable ecosystems. Regulatory compliance enables the adoption of high-efficiency dewatering agents that break down colloidal structures in sludge, improving solid-liquid separation and reducing municipal waste volume. The environmental mandates support a sludge treatment chemicals market for stabilizers and disinfectants that neutralize heavy metals and industrial waste to achieve strict safety standards.

Restraint

Volatility and High Cost of Raw Material

A major obstacle to market growth is reliance on petroleum-based feedstocks for polymers and conditioning agents, as their costs linked to the volatile oil market cause supply disruptions and higher treatment costs. High capital expenses for modern dosing systems further strain budgets, often forcing utilities to stick with outdated, less efficient methods because switching to high-purity chemicals is too costly for emerging facilities.

Opportunity

The Transition Towards the Biorefineries

The sludge treatment chemicals market is transforming sludge treatment facilities into resource recovery hubs by accelerating the commercial opportunity to advance chemicals for selective mineral extraction and nutrient harvesting. This opportunity is driving the manufacturing of sustainable organic fertilizers by separating phosphorus and nitrogen waste for treatment infrastructure. The global push for carbon neutrality is fueling the demand for renewable biopolymers and environmentally friendly chemicals. Additionally, chemical suppliers can lead the sludge-to-energy transition by developing conditioners that boost methane production during digestion, thereby converting sludge into a renewable energy source.

Segmental Insights

Product Type Insights

The flocculants segment dominated the market with the largest share of 34% in 2025. Flocculants are categorized as anionic, cationic, and non-ionic flocculants, which are essential for solid-liquid separation by promoting fast sedimentation. These products act as high-molecular-weight polymers that bind particles into large, durable cohesive flocs, clarifying water efficiently. The sludge treatment chemicals market preferred custom-charged polyacrylamides for waste streams. Flocculants increase operational value and enable treatment facilities to process higher sludge volumes by ensuring high workflow and water clarity.

")

The dewatering aids segment held the 11% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period. Function as chief surfactants that re-engineer water's bond with sludge particles. The organic and inorganic dewatering agents have lower logistical costs, labor, and transport expenses. By lowering capillary suction time and surface tension, trapped moisture is removed during compression. Dewatering aids maximize solids concentration, producing a hair dryer, lighter waste for plant operators, aligning with modern formulations, boosting the market growth.

Sludge Treatment Chemicals Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Flocculants | 34% |

| Coagulants | 26% |

| Disinfectants | 8% |

| Conditioning Chemicals | 12% |

| Dewatering Aids | 11% |

| Stabilization Chemicals | 6% |

| Others | 3% |

Sludge Type Insights

The municipal sludge segment dominated the market with the largest share of 49% in 2025, generated from urban sanitation and household waste due to its large sludge volumes and operational complexity. The government focuses on pathogen inactivation and odor neutralization, transforming hazardous municipal waste into safe biosolids by preventing landfilling. The operator converts utility sludge into an agricultural resource by neutralizing heavy metals and drug residues. The merging trend is driving the treatment transformation by adopting resource recovery to promote circular urban infrastructure.

The industrial sludge segment held 39% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period. It is created by a diversified chemical industry, including toxic synthetic compounds from textiles, mining, food, refining, and the pulp & paper industry. The industrial sludge contains emulsified hydrocarbons, heavy metallic element, and resistant organic pollutants that requires specialized advanced chemical treatments. This segment is supported by emulsion-breaking agents and high-purity precipitants to reduce pH fluctuations and toxicity. Managing industrial sludge is vital for mitigating risks and preventing.

Sludge Treatment Chemicals Market Share, By Sludge Type, 2025 (%)

| By Sludge Type | Revenue Share, 2025 (%) |

| Municipal Sludge | 49% |

| Industrial Sludge | 39% |

| Hazardous Sludge | 12% |

Treatment Process Insights

The dewatering segment dominated the market with the largest share of 31% in 2025, because of the requirement for cost-efficiency and sludge volume reduction in sludge management. This treatment process enables precise chemical dosing to maximize filter press, belt press, and centrifuge efficiency. The advancement of sensor-driven systems that monitor sludge density and adjust chemical injection in real-time to prevent over-treatment. The manufacturer seeks thermal drying, incineration, and land application, making dewatering more energy-driven and cost-efficient by enhancing the treatment hub's economic viability.

") The digestion segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 7.30% over the forecast period. Chemicals function as biochemical catalysts, breaking down cellular membranes and proteins to make organic carbon for methane-producing bacteria. Digestion is a complex biological process that recovers methane and enhances energy insufficiency. This pre-treatment accelerates biogas production and transforms treatment infrastructure into renewable energy biorefineries. The sludge treatment chemicals make solids nutrient-rich and safe for processing for agricultural use. The major investor focuses on improving the efficiency of aerobic and anaerobic digestion to boost market expansion.

The digestion segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 7.30% over the forecast period. Chemicals function as biochemical catalysts, breaking down cellular membranes and proteins to make organic carbon for methane-producing bacteria. Digestion is a complex biological process that recovers methane and enhances energy insufficiency. This pre-treatment accelerates biogas production and transforms treatment infrastructure into renewable energy biorefineries. The sludge treatment chemicals make solids nutrient-rich and safe for processing for agricultural use. The major investor focuses on improving the efficiency of aerobic and anaerobic digestion to boost market expansion.

Sludge Treatment Chemicals Market Share, By Treatment Process, 2025 (%)

| By Treatment Process | Revenue Share, 2025 (%) |

| Thickening | 14% |

| Conditioning | 17% |

| Dewatering | 31% |

| Stabilization | 13% |

| Digestion | 15% |

| Drying | 10% |

Application Insights

The municipal wastewater treatment segment dominated the market with the largest share of 46% in 2025. This application focuses on large-scale urban waste remediation to shield aquatic ecosystems and support water reclamation. Municipal wastewater treatment requires the use of coagulants and disinfectants to meet safety standards and protect public health, thereby promoting the circular economy. An emerging country is increasingly inclined towards nutrient harvesting, which uses chemicals to remove phosphorus and nitrogen by preventing eutrophication. Additionally, the government focuses on smart water infrastructure and the digitization of chemicals to maintain cost efficiency.

The industrial wastewater treatment segment held the 31% market share in 2025 and is expected to grow at the fastest CAGR of 7.2% over the forecast period. This sector demands sludge treatment chemicals to neutralize a broad spectrum of contaminants, including pharmaceutical residues, synthetic dyes, and acidic mine drainage. The manufacturers focus on chemical solutions to remove specific pollutants from various factory processes. The move towards achieving zero liquid discharge, where chemicals purify process water for reuse, is integrated with a closed-loop system. Advanced chemical treatment is a strategic solution that supports wastewater operations and sustainable manufacturing practices to meet regulatory compliance.

Sludge Treatment Chemicals Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Municipal Wastewater Treatment | 46% |

| Industrial Wastewater Treatment | 31% |

| Drinking Water Treatment Residuals | 7% |

| Septage Treatment | 5% |

| Resource Recovery & Reuse | 6% |

| Landfill Management | 3% |

| Others | 2% |

End-Use Industry Insights

The municipal utilities segment dominated the market with the largest share of 42% in 2025.Function as the prime consumers of sludge treatment chemicals that offer long-term process stability and regulations with health standards supporting public sanitation infrastructure. Municipal utilities are moving toward a smart city framework by adopting digital platforms and automation to optimize sludge impurity and reduce costs. The large-scale municipal operations focus on sustainable bio-polymers and green chemistry, making them an industry leader by providing a stable supply chain.

The chemicals & petrochemicals segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period and driven by the requirement for advanced stabilization and remediation to eliminate volatile and hazardous sludge. Petrochemicals focuses on managing resistant hydrocarbons, oily emulsions, and synthetic pollutants through oxidation processes and high-purity conditioners to meet stringent environmental standards. The chemical & petrochemical industry's demand for efficient sludge treatment is vital for operational resilience, sustainability, and for recovering valuable hydrocarbons while reducing treatment costs and maintaining ESG compliance.

Sludge Treatment Chemicals Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Municipal Utilities | 42% |

| Food & Beverage | 11% |

| Pulp & Paper | 10% |

| Chemicals & Petrochemicals | 12% |

| Mining & Metals | 8% |

| Pharmaceuticals | 5% |

| Textile Industry | 5% |

| Power Generation | 4% |

| Others | 3% |

Regional Insights

How Did the Asia Pacific Dominated the Sludge Treatment Chemicals Market in 2025?

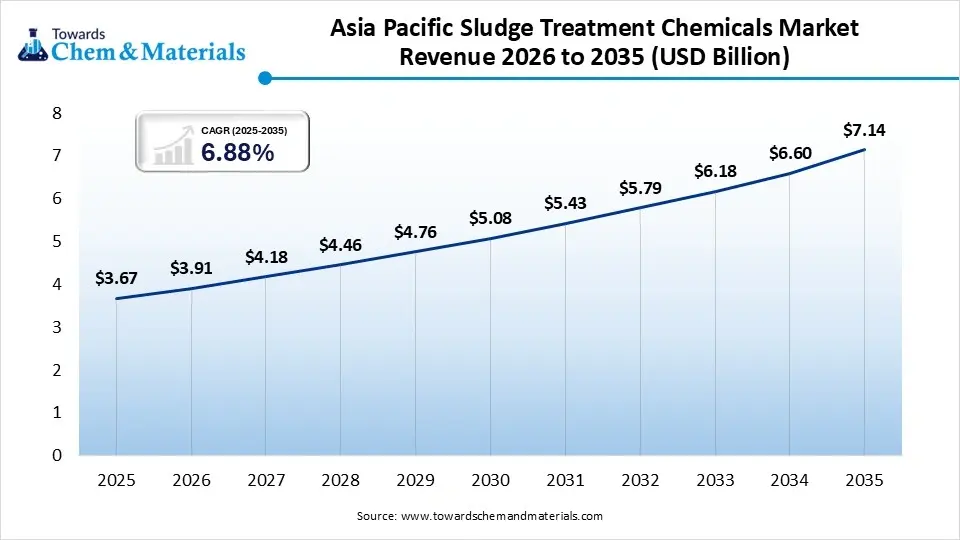

The Asia Pacific sludge treatment chemicals market size was estimated at USD 3.67 billion in 2025 and is projected to reach USD 7.14 billion by 2035, growing at a CAGR of 6.88% from 2026 to 2035.Asia Pacific dominated the market by holding 38% share in 2025, driven by urban infrastructure and industrial expansion. The regional regulatory framework involves water conservation laws by boosting the shift towards advanced zero liquid discharge systems. Government support for smart cities promotes automated chemical dosing and helps municipal utilities with waste management. The domestic electronics and textile industry focuses on treating effluents to reduce sludge volume and protect water sources across the Asia Pacific.

China

China

- Driven by a government-led push to upgrade treatment facilities and associated with the 14th Five-Year Plan, China promotes zero liquid discharge to conserve freshwater.

- Additionally, domestic expansion is boosted by phosphorus harvesting for rapid dewatering in textiles and electronics industries by implementing ecological redlines that limit the discharge of untreated industrial sludge.

India

- India's urban growth demands high-purity chemical treatments, municipal waste cleanup, and advanced effluent treatment through government support.

- Domestic players using high-solid-content polyacrylamides, odor-control, and stabilizers for food processing and pharmaceutical hubs.

The North America sludge treatment chemicals market size was estimated at USD 2.41 billion in 2025 and is projected to reach USD 4.73 billion by 2035, growing at a CAGR of 6.98% from 2026 to 2035.North America held the 25% market share in 2025 and is expected to grow at the fastest with a CAGR of 7.60% during the forecast period, serving as a technological innovation and stringent environmental regulations. There's a shift toward energy-positive treatment facilities with pre-treatment of organic matter to accelerate methane manufacturing in digesters. Regional stakeholders focus on the confiscation of persistent organic pollutants, especially PFAS, using advanced oxidation and chemical stabilizers. North America's growth is fostered by corporate sustainability goals and ESG investments, which promote IoT monitoring and digital analytics to optimize chemical use and help meet EPA biosolids regulations.

United States

- US focus on sludge-to-energy for energy-neutral utilities. The environmental protection and biosolids mandates stabilization and pathogen removal for the agricultural and municipal sectors.

- Domestic growth is driven by national efforts to remove PFAS from sludge and move towards digital water management using AI for ESG investment and transparency.

Canada

- The rising demand for eco-friendly and bio-based polymers that lower toxicity during waste treatment to meet wastewater system effluent regulation and stricter nutrient removal compliance.

- Canada focuses on cold-water ecosystems for domestic treatment and reclamation through substantial investments.

The Europe sludge treatment chemicals market size was estimated at USD 2.32 billion in 2025 and is projected to reach USD 4.54 billion by 2035, growing at a CAGR of 14.46% from 2026 to 2035.Europe held the 24% market share in 2025. Leading in circular waste management and resource harvesting through the Green Deal. The region implementing green chemistry is driving innovation in bio-based, biodegradable flocculants and recovery of phosphorus into sustainable fertilizers. The limited landfill space and stringent regulations underscore the need for European plants to use high-efficiency dewatering aids to enable energy-efficient incineration. The domestic move towards nutrient recycling and toxin reduction makes Europe a hub for achieving zero-pollution and carbon-neutrality goals.

Germany

- The country observed the transition towards mineral independence and the use of high-efficiency conditioning agents to meet legislation mandates phosphorus recovery from sludge and improve thermal recycling

- German players focus on the extraction of high-purity minerals, which boosts the opportunity for developing recovery catalysts and advanced chemical extraction.

The Latin America sludge treatment chemicals market size was estimated at USD 0.68 billion in 2025 and is projected to reach USD 1.39 billion by 2035, growing at a CAGR of 7.41% from 2026 to 2035.Latin America held the 7% market share in 2025. Driven by mining and agricultural networks, demand for sludge treatment chemicals is supported by government initiatives and sanitation modernization. Latin America is upgrading to polymeric conditioners for wastewater treatment, offering significant opportunities for innovative formulations. The region focuses on odor control and pathogen reduction in emerging cities, integrating advanced dewatering technology to meet climate and environmental standards.

Brazil

- The expansion is supported by private capital investment for pathogen neutralization and a legal framework for sanitation and waste treatment

- Brazil uses high-affinity flocculants in industrial and municipal applications to meet industrial discharge limits and safety standards.

Chile

- The domestic revolution toward remediation of toxic mining tailing sludge enables the implementation of high salinity coagulants and water-recovery additives.

- The Chile regulatory infrastructure focuses on mining safety and chemical stabilization to prevent contamination, fueling the domestic growth.

The Middle East and Africa sludge treatment chemicals market size was estimated at USD 0.58 billion in 2025 and is projected to reach USD 1.21 billion by 2035, growing at a CAGR of 7.63% from 2026 to 2035.The Middle East & Africa held the 6% market share in 2025, due to a regional move toward water independence and expanding public sanitation in Gulf high-tech economies. The domestic players demand wastewater reclamation, emulsion breakers, and high-purity conditioners for regional cooling, petrochemical, and desert agriculture. In Africa, expansion is driven by new municipal wastewater systems serving urban populations, which use coagulants and stabilizers to remove pathogens. MEA governments' initiatives for circular economy goals, transforming hazardous sludge into renewable biogas and soil conditioners.

") Saudi Arabia

Saudi Arabia

- The domestic expansion is supported by the Vision 2030 initiative and desert afforestation to achieve the water strategy and the standards for treated sewage effluents.

- The county is witnessing a rising use of high-purity conditioners and cost-effective coagulants through large-scale greening projects.

Competitive Landscape Analysis

Tier 1 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

| 1 | Kemira Oyj | Helsinki, Uusimaa | Finland | One of the world's largest suppliers of sludge dewatering and wastewater treatment chemicals with strong municipal and industrial presence | Polyacrylamide flocculants, ferric salts, coagulants, sludge dewatering chemicals |

| 2 | SNF Group | Andrézieux-Bouthéon, Loire | France | Global leader in polyacrylamide production and sludge treatment polymers | Flocculants, cationic/anionic polymers, sludge conditioning agents |

| 3 | BASF SE | Ludwigshafen, Rhineland-Palatinate | Germany | Major producer of performance polymers used in sludge thickening and dewatering applications | Zetag® flocculants, coagulants, wastewater treatment polymers |

| 4 | Solenis LLC | Wilmington, Delaware | United States | Leading specialty chemical company serving municipal and industrial wastewater treatment markets | Flocculants, coagulants, sludge dewatering aids, conditioning chemicals |

| 5 | Ecolab Inc. (Nalco Water) | Saint Paul, Minnesota | United States | Global water treatment leader with extensive sludge management and wastewater chemical portfolio | Nalco™ flocculants, coagulants, sludge conditioners, treatment chemicals |

Tier 2 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

| 1 | Kurita Water Industries Ltd. | Tokyo | Japan | Major industrial water treatment company with strong sludge reduction and treatment capabilities | Coagulants, sludge conditioners, wastewater treatment chemicals |

| 2 | Veolia Water Technologies | Aubervilliers, Île-de-France | France | Integrated wastewater treatment provider offering sludge treatment chemicals and process solutions | Sludge conditioning reagents, dewatering chemicals, treatment additives |

| 3 | SUEZ Water Technologies & Solutions | Trevose, Pennsylvania | United States | Significant participant in wastewater and biosolids treatment markets | Flocculants, coagulants, sludge processing chemicals |

| 4 | Feralco Group | Helsingborg, Skåne County | Sweden | Major European producer of inorganic coagulants used extensively in sludge treatment | Ferric chloride, aluminum sulfate, polyaluminum chloride |

| 5 | Chemtrade Logistics Inc. | Toronto, Ontario | Canada | Leading producer of inorganic coagulants widely used in municipal sludge treatment operations | Ferric sulfate, ferric chloride, aluminum-based coagulants |

Tier 3 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

| 1 | Beckart Environmental, Inc. | Kenosha, Wisconsin | United States | Specialized wastewater and sludge treatment chemical supplier serving industrial customers | Flocculants, coagulants, sludge conditioning chemicals |

| 2 | Aries Chemical, Inc. | Beaver Falls, Pennsylvania | United States | Focused supplier of wastewater and biosolids treatment chemicals | Ferric salts, coagulants, sludge treatment products |

| 3 | Accepta Ltd. | Bradford, England | United Kingdom | Regional specialist in wastewater treatment and sludge dewatering chemicals | Flocculants, coagulants, sludge dewatering polymers |

| 4 | BWA Water Additives UK Ltd. | Manchester, England | United Kingdom | Specialty water treatment chemical company with growing wastewater portfolio | Performance flocculants, coagulants, treatment additives |

| 5 | Ixom Operations Pty Ltd. | Melbourne, Victoria | Australia | Important regional supplier of water and wastewater treatment chemicals in Asia-Pacific | Alum, ferric chloride, polyaluminum chloride, sludge treatment chemicals |

- The competitive landscape is transforming the sludge treatment chemicals market through molecular innovation, and digital integration is crucial for securing long-term municipal and industrial agreements.

- BASF and Kemira move towards performance-based contracts, Ecolab (Nalco Water) centrals by installing sensors for real-time and autonomous dosing.

- SNF Group and Solenis focus on green technology with plant-based flocculants to achieve carbon-neutral targets and sustainability aims.

Recent Developments

- In September 2025, SUS ENVIRONMENT showcased cutting-edge Waste-to-Energy (WtE) and AI-Twin Digital technologies at the Waste Management Association of Malaysia conference, highlighting real-time digital waste treatment models and receiving recognition for sustainable waste management leadership.(Source: prnewswire)

- SUEZ and CNRS Research Framework (Renewal through 2030): In April 2025, SUEZ and CNRS formalized a five-year R&D partnership focused on innovative research in water and waste management. This strategy promotes sustainable resource management and advanced decarbonization technologies.(Source: smartwatermagazine)

Top Companies in the Sludge Treatment Chemicals Market and Their Offerings

- Kemira Oyj: The leader in integrating high-performance organic coagulants and, through its digital platforms, is adopting automated polymer dosing. This company maintains its leadership in the municipal sector by providing operational cost-effectiveness.

- BASF SE: a provider of high-performance flocculation solutions that focuses on eco-friendly innovation by utilizing the biomass balance production model to meet ESG reporting standards.

- AkzoNobel

- Ashland

- Shandong

- DowDuPont

- Ecolab Inc.

- Lonza

- Suez S.A.

- Kurita Water Industries Ltd.

- Buckman Laboratories International Inc.

- Feralco Group

- ChemTreat, Inc.

- Solenis LLC

- Accepta Ltd.

- Thermax Limited

- Veolia Water Technologies & Solutions

Segments Covered in the Report

By Product Type

- Flocculants

- Anionic Flocculants

- Cationic Flocculants

- Non-Ionic Flocculants

- Coagulants

- Aluminum-Based Coagulants

- Iron-Based Coagulants

- Organic Coagulants

- Disinfectants

- Chlorine-Based

- Peracetic Acid-Based

- Ozone-Based

- Conditioning Chemicals

- Lime

- Ferric Salts

- Polymer Conditioners

- Dewatering Aids

- Organic Dewatering Agents

- Inorganic Dewatering Agents

- Stabilization Chemicals

- Alkaline Stabilizers

- Oxidizing Stabilizers

- Others

- Odor Control Chemicals

- Nutrient Removal Chemicals

By Sludge Type

- Municipal Sludge

- Primary Sludge

- Secondary Sludge

- Mixed Sludge

- Industrial Sludge

- Chemical Industry Sludge

- Food & Beverage Sludge

- Pulp & Paper Sludge

- Textiles Sludge

- Mining Sludge

- Hazardous Sludge

- Petrochemical Sludge

- Pharmaceutical Sludge

- Metal Processing Sludge

By Treatment Process

- Thickening

- Gravity Thickening

- Flotation Thickening

- Conditioning

- Chemical Conditioning

- Thermal Conditioning

- Dewatering

- Belt Filter Press

- Centrifuge

- Filter Press

- Stabilization

- Lime Stabilization

- Chemical Stabilization

- Digestion

- Aerobic Digestion

- Anaerobic Digestion

- Drying

- Thermal Drying

- Solar Drying

By Application

- Municipal Wastewater Treatment

- Industrial Wastewater Treatment

- Drinking Water Treatment Residuals

- Septage Treatment

- Resource Recovery & Reuse

- Landfill Management

- Other

By End-Use Industry

- Municipal Utilities

- Food & Beverage

- Pulp & Paper

- Chemicals & Petrochemicals

- Mining & Metals

- Pharmaceuticals

- Textile Industry

- Power Generation

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Tags

FAQ's

Select User License to Buy

Figures (8)