Content

What is the Current Size of the Ductless HVAC Systems Market and Its Projected Growth?

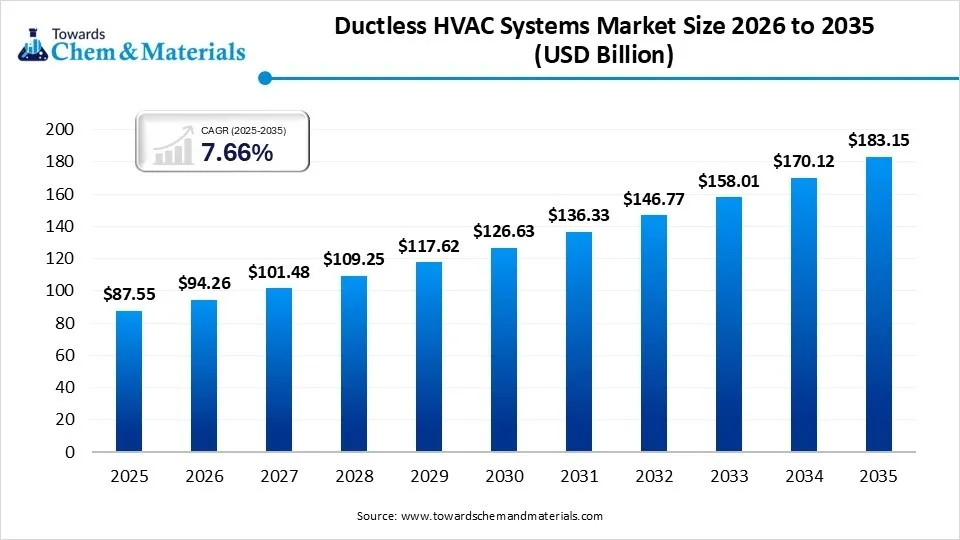

The global ductless HVAC systems size was estimated at USD 87.55 billion in 2025 and is expected to increase from USD 94.26 billion in 2026 to USD 183.15 billion by 2035, growing at a CAGR of 7.66% from 2026 to 2035. Asia Pacific dominated the ductless HVAC systems with the largest revenue share of 48.00% in 2025.The market expansion is driven by net-zero building targets, decarbonization, rising eco-conscious consumers, shift towards low-GWP refrigerants and electrification.

")

Market Highlights

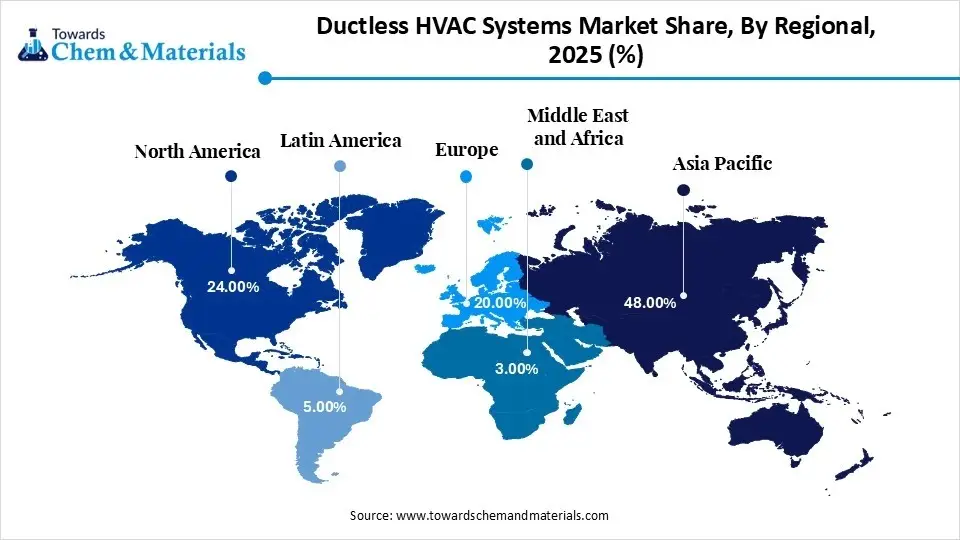

- By region, Asia Pacific dominated the ductless HVAC systems market share 48.00% in 2025 due to its rapid urbanization and adoption of inverter technology.

- By region, North America is expected to grow at the fastest CAGR from 2026 to 2035 due to the shift towards electrification and a carbon-neutral residential framework.

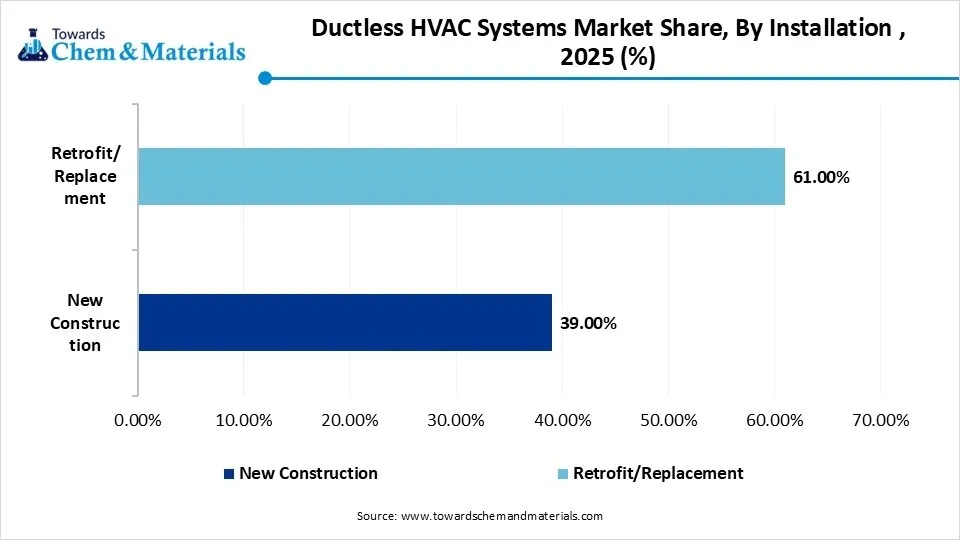

- By installation, the retrofit/replacement segment held the largest share in the market in 2025 due to modernization and demand for non-invasive installation.

- By installation, the new construction segment is expected to grow at the fastest CAGR during the forecast period due to its system-spread efficiency and spatial optimization.

- By equipment type, the air conditioners segment dominated the market, driven by inverter compressors and their single-function cooling.

- By equipment type, the heat pump segment is expected to grow at the fastest CAGR in the market during the forecast period due to its dual function and demand for modern, sustainable climate solutions.

- By end-use, the residential segment dominated the market due to its consumer demand for personalized control and shift towards residential decarbonization.

- By end-use, the commercial segment is anticipated to grow at the fastest CAGR in the market during the forecast period due to its operational scalability and precise climate control.

Market Overview

Ductless HVAC systems are a high-growth sector driven by decarbonization and electrification that offers decentralized climate solutions with zonal cooling and heating. The market is driven by the adoption of inverter technology for variable-speed operations. The integration of smart systems with IoT-based sensors and AI diagnostics for real-time monitoring.

The increasing adoption of commercial and residential buildings, along with retrofit upgrades for traditional buildings to meet modern efficiency standards. As ecological regulations tighten, ductless units are vital to the net-zero building movement due to high seasonal energy efficiency ratings and electric operation.

Recent Market Trends

- Rising Focus on Decarbonization: The market is shifting towards structural transformation as high-performance heat pumps replace fossil-fuel combustion systems, enabling building-level carbon neutrality and lowering direct emissions.

- Grid-Cooperative Energy Management: The systems are increasingly designed with smart-grid communication modules that act as distributed energy resources with domestic renewable energy sources to meet electrical loads.

- Shift Towards Sustainable Refrigerant: The stringent regulatory framework is pushing the industry towards low-GWP refrigerants that integrate with tightening environmental sustainability and climate mandates.

- Rising Demand for Indoor Air Purification: The demand for multi-stage filtration systems that integrate with HEPA technology and UV-C sterilization, converting HVAC units to medical-grade infrastructure.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 94.26 Billion |

| Revenue Forecast in 2035 | USD 183.15 Billion |

| Growth Rate | CAGR 7.66% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Installation, By Equipment Type, By End-Use, By Region |

| Key companies profiled | Daikin Industries Ltd., Mitsubishi Electric Corporation, Fujitsu General Limited, LG Electronics, Samsung Electronics, Panasonic Corporation, Carrier; Trane Technologies plc, Lennox International Inc., Rheem Manufacturing Company, Gree Electric Appliances Inc., Bosch Thermotechnology, Haier Smart Home Co., Ltd., Midea Group, Johnson Controls International plc. |

Key Technological Shifts and AI in the Ductless HVAC Systems Market

Technological transformation and AI integration are defined by their advanced ductless HVAC systems as an intelligent energy asset. The industrial revolution of inverter-based technology to maintain peak operational performance. Predictive maintenance is transforming these systems into smart technology, which includes variable compressor speeds, occupancy detection, and smart sensor integration. These ductless HVAC systems support demand-response programs and smart-grid interaction to stabilized electrical grid, positioning the technological shift as central to autonomous and efficient building infrastructure.

Ductless HVAC Systems Market: Supply Chain Analysis

- Manufacturing of Core Components: The stage of conversion of raw materials into key components like compressors, evaporator coils, and indoor and outdoor units. The stage involves integration of IoT sensors and Wi-Fi-based thermostats with smart home systems.

- Key Players: Daikin Industries Ltd., Carrier Global Corporation, LG Electronics, Gree Electric and Mitsubishi Electric Corporation

- Logistics and Specialized Channels: The stage of managing complex logistics and technical training for the installation of specialized ductless HVAC systems. The indirect and direct channels provide inventory management and exploring direct-to-consumer models for installers.

- Key Players: Watsco, Inc., Ferguson plc., Johnstone Supply, Lennox International, Midea and Carrier

- Service and Installation: The final stage of HVAC licensed contractors, retailers that sell and install systems for specialized applications, with proper aftermarket and maintenance that drives consumer and residential adoption.

- Key Players: iCool, Ubuy, Aries Energy, Adunik Powetech and ARSTECH

Regulatory Framework: Ductless HVAC Systems Market

| Region | Key Regulation | Regulatory Focus |

| International | Kingali Amendment | The global legal framework is driven by a shift towards eco-friendly refrigerants for lower global warming potential chemistries. |

| North America | AIM Act and DOE M1Standards | Phasing out HFC refrigerants to ensure ductless units perform efficiently under real-world residential loads. |

| China | GB Standards | Mandates minimum energy efficiency standards for room air conditioners align with carbon neutrality commitments. |

| Asia Pacific | Energy Conservation Building Codes | Focus on mandatory inverter technology for urban development to balance peak power demands in high-density tropical cities. |

| United States | Inflation Reduction Act | Transformative tax credits to offset the cost of residential electrification to boost heat pump adoption. |

| Europe | F-Gas Regulation | Banning small ductless units with high-GWP gases is forcing a shift towards natural refrigerants. |

| Germany | Building Energy Act | Requirements for newly installed heating systems to be the least renewable energy and primary compliance solution for residential retrofits. |

Segmental Insights

Installation Insights

Retrofit/Replacement Segment Dominated The Ductless HVAC Systems Market In 2025

The retrofit/replacement segment dominated the market in 2025, driven by modernization and sustainability in a well-established framework. The segment is preferred for decarbonization, replacing old fossil-fuel furnaces with electric heat pumps. Its main advantage is the non-invasive installation, avoiding costs and engineered disruptions of traditional ductwork. The rising shift emphasises zonal efficiency, enabling modular climate control in the high-use sector while keeping operational costs low. The key innovations include inverter compressors and smart-grid compatibility to meet Net-Zero energy ratings. Additionally, the dominance of retrofits is accelerated by consumers' demand for quiet operation and advanced air filtration to meet environmental standards.

")

The new construction segment is the fastest-growing in the market during the forecast period, The new construction segment leads because it offers system-spread efficiency and space optimization, driving implementation of all-electric, modular systems over traditional ducted infrastructure. It integrates multi-zone technology, concealed cassettes, and slim ducts for a simple aesthetic. This segment aligns with smart home automation and an AI-driven ecosystem, enabling real-time energy use. It supports the shift toward Net-Zero standards, leveraging high SEER ductless units to improve sustainability. The rising demand for decentralized heating and cooling reduces thermal leakage, making the segment the preferred choice for modern architectural design.

Ductless HVAC Systems Market Share, By Installation , 2025 (%)

| By Installation | Revenue Share, 2025 (%) |

| New Construction | 39.00% |

| Retrofit/Replacement | 61.00% |

- New Construction segment accounts for 39% of the market share, driven by the growing demand for energy-efficient and space-saving HVAC systems in newly built residential and commercial buildings, but not dominating due to competition from retrofit solutions.

- Retrofit/Replacement segment holds 61% of the market share, dominating due to the large number of older buildings requiring system upgrades for better efficiency and performance, making it the preferred choice for many consumers.

Equipment Type Insights

The Air Conditioners Segment Led The Ductless HVAC Systems Market In 2025 With The Largest Share

The air conditioners segment held the largest revenue share in the market in 2025. The segment offers single-function cooling for dry climates and high-heat climates where cooling demand outpaces heating. The segment is driven by inverter compressors and IoT sensors that improve efficiency and temperature control, align with smart and variable-speed operation. Additionally, air conditioners are cost-effective, with a high energy efficiency ratio and a simple aesthetic, providing modular cooling solutions that avoid duct thermal losses.

The heat pump segment is experiencing the fastest growth in the market during the forecast period. Offering dual-function heating and cooling. It drives electrification, replacing fossil fuels with high-efficiency thermal transfer. The technological integration in this segment, with hyper-heating and inverter compressors, ensures performance in extreme temperatures. As a ductless HVAC system, it supports decarbonization and net-zero building initiatives with a high coefficient of performance, zonal energy management, and AI diagnostics that strengthen the segment position in next-generation sustainable climate solutions.

Ductless HVAC Systems Market Share, By Equipment Type , 2025 (%)

| By Equipment Type | Revenue Share, 2025 (%) |

| Air Conditioners | 42.00% |

| Heat Pump | 28.00% |

| Dehumidifiers | 30.00% |

- Air Conditioners segment accounts for 42% of the market share, dominating due to their widespread use in both residential and commercial applications, where cooling is the primary need.

- Heat Pump segment holds 28% of the market share, gaining momentum as a versatile option for both heating and cooling, but not dominating due to its higher installation costs compared to air conditioners.

- Dehumidifiers segment represents 30% of the market share, used for moisture control in indoor environments, but not dominating due to its more specialized role in specific regions and applications.

End-Use Insights

The Residential Segment Dominated The Ductless HVAC Systems Market In 2025

The residential segment dominated the market in 2025, driven by massive consumer demand for personalized climate control. The segment focuses on residential decarbonization, with homeowners replacing old systems with multi-zone heat pumps for precise control. The growing preference for whisper-quiet operation, minimalist design, and smart home infrastructure is boosting the market adoption by integration with AI and IoT sensors. This system enhances indoor air quality and efficiency, establishing ductless systems as the standard for premium and sustainable living.

The commercial segment is anticipated to grow fastest in the market during the forecast period, value for its operational scalability and precise control over climate. As innovators moving away from energy-heavy central chillers to VRF and multi-split heat pumps to promote commercial decarbonization, accelerating the segmental growth. It emphasizes zonal efficiency, allowing independent temperature management and reducing utility costs. The integration of building management systems and IoT solutions enables performance optimization and predictive maintenance. Additionally, these systems help the commercial sector accomplish net-zero standards aligned with corporate sustainability mandates, making them the leading choice for sustainable infrastructure.

Ductless HVAC Systems Market Share, By End-use, 2025 (%)

| By End-use | Revenue Share, 2025 (%) |

| Residential | 54.00% |

| Commercial | 26.00% |

| Industrial | 20.00% |

- Residential segment accounts for 54% of the market share, dominating due to the high demand for energy-efficient and space-saving solutions in homes, particularly in areas with varying climates.

- Commercial segment holds 26% of the market share, driven by the need for efficient and flexible HVAC systems in offices, retail, and other business establishments, but not dominating due to the larger share of residential applications.

- Industrial segment represents 20% of the market share, used in large-scale industrial operations where climate control is critical, but not dominating due to the smaller size of this segment compared to residential and commercial applications

Regional Insights

The Asia Pacific ductless HVAC systems market size was valued at USD 42.02 billion in 2025 and is expected to be worth around USD 88.83 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 7.77% over the forecast period from 2026 to 2035. Asia Pacific dominated the market share 48.00% in 2025, driven by Inverter Technology and urban energy efficiency. The region is a key driver of electric infrastructure that prefers space-saving climate solutions. The region is shifting toward high-efficiency heat pumps and VRF systems integrated into smart city infrastructure. Rising environmental concerns are driving the adoption of Low-GWP refrigerants to meet environmental standards and net-zero buildings in the domestic ecosystem. By emphasising modular and zonal cooling, the Asia Pacific sets the global standard for advanced climate control and a sustainable framework.

")

China Ductless HVAC Systems Market Growth Trends

China maintain leadership in the market due to its manufacturing and consumer base, supported by decarbonization commitments and rapid urbanization. The region leads in Inverter Technology and VRF systems, while the shift is toward all-electric heating, with high-performance heat pumps supporting regional net-zero targets. The widespread use of Smart-HVAC ecosystems with digital transformation enables regional growth. China defines targets for sustainable climate control and low-GWP refrigerant promoted by government incentives and consumer demand for air quality.

North America Ductless HVAC Systems Market Growth Trends

North America is expected to grow at the fastest CAGR in the market during the forecast period, driven by electrification and carbon-neutral residential organization. The region maintains its dominance in cold-climate heat pumps, replacing fossil fuels due to their performance in extreme temperatures. The rising retrofit installations are complemented by smart-grid and AI energy management for grid communication, which is fueling the domestic expansion. The local incentives and national policies for high-efficiency systems make North America's transition towards low-GWP refrigerants and inverter technology for sustainable building upgradation.

U.S. Ductless HVAC Systems Market Growth Trends

The United States market is a pillar of residential electrification, driven by a shift toward low-carbon building infrastructure. National incentives focus on the replacement of fossil fuels with high-performance cold-climate heat pumps. Additionally, the U.S. based homeowners are implementing retrofit systems for zonal control and energy efficiency that integrate into smart homes. The domestic manufacturers focus on low-GWP refrigerants and inverter technology, positioning the U.S. leadership for energy efficiency and the Net-Zero housing movement.

")

Europe Ductless HVAC Systems Market Growth Trends

Europe market is witnessing growth during the notable period due to decarbonization and renewable integration for HVAC that reinforced by strict environmental laws. The region is transitioning to natural refrigerants and low-GWP alternatives, with air-to-air heat pumps as the main residential heating method. Europe's smart-grid integration helps optimize energy use based on real-time electricity and renewables. As the industry focuses on net-zero buildings and leverages inverter technology and AI thermal management to maximize SCOP, making ductless systems vital for European energy security.

Ductless HVAC Systems Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 24.00% |

| Europe | 20.00% |

| Asia Pacific | 48.00% |

| Latin America | 5.00% |

| Middle East & Africa | 3.00% |

Germany Ductless HVAC Systems Market Growth Trends

Germany market serves as a catalyst for the energy transition, which is supported by the nation-building energy act. The region advances in natural refrigerants, notably propane (R-290), with high-efficiency heat pumps that meet urban noise standards. The regional adoption of smart-grid interactivity improves energy autonomy through grid synchronization and photovoltaic integration. Germany is shifting toward fossil-free infrastructure and relies on inverter technology and energy-efficient labelling to promote ductless systems as key to energy independence and sustainable construction.

Recent Developments

- In September 2025, Bosch Home Comfort Group launched the Hitachi airHome series, which includes single and multi-room ductless heat pumps with smart connectivity and self-cleaning technology. This new launch helps homeowners to lower heating and cooling costs.(Source: www.bosch-presse.de)

- In May 2024, Samsung Electronics announced the formation of a joint alliance with Lennox with the title Samsung Lennox HVAC North America for ductless and variable refrigerant flow HVAC systems in the United States and Canada. This venture focuses on selling ductless mini-split and VRF products in the U.S. and Canada.(Source: news.samsung.com)

Top Companies in the Ductless HVAC Systems Market and Their Offerings

- Mitsubishi Electric Corporation: The major player specializes in high-efficiency ductless mini-split and multi-split systems with the FS-series. They set a standard for cold-climate performance through their hyper-heating technology.

- Dalkin Industries Ltd.: The global leader of variable refrigerant volume offers a quaternity series and inverter-driven swing compressors with higher operational longevity and performance, preventing friction and vibration.

- Gree Electric Appliances Inc.: The global manufacturer of Gree Sapphire Series and its proprietary G10 inverter technology to operate ultra-low frequencies and achieve leading SEER ratings up to 38.

- Fujitsu General Limited

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Carrier

- Trane Technologies plc

- Lennox International Inc.

- Rheem Manufacturing Company

- Bosch Thermotechnology

- Haier Smart Home Co., Ltd.

- Midea Group

- Johnson Controls International plc

Segment Covered in the Report

By Installation

- New Construction

- Retrofit/Replacement

By Equipment Type

- Air Conditioners

- Heat Pump

- Dehumidifiers

By End-Use

- Residential

- Commercial

- Industrial

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)