Content

Asia Pacific Metal Casting Market Size and Forecast 2026 - 2035

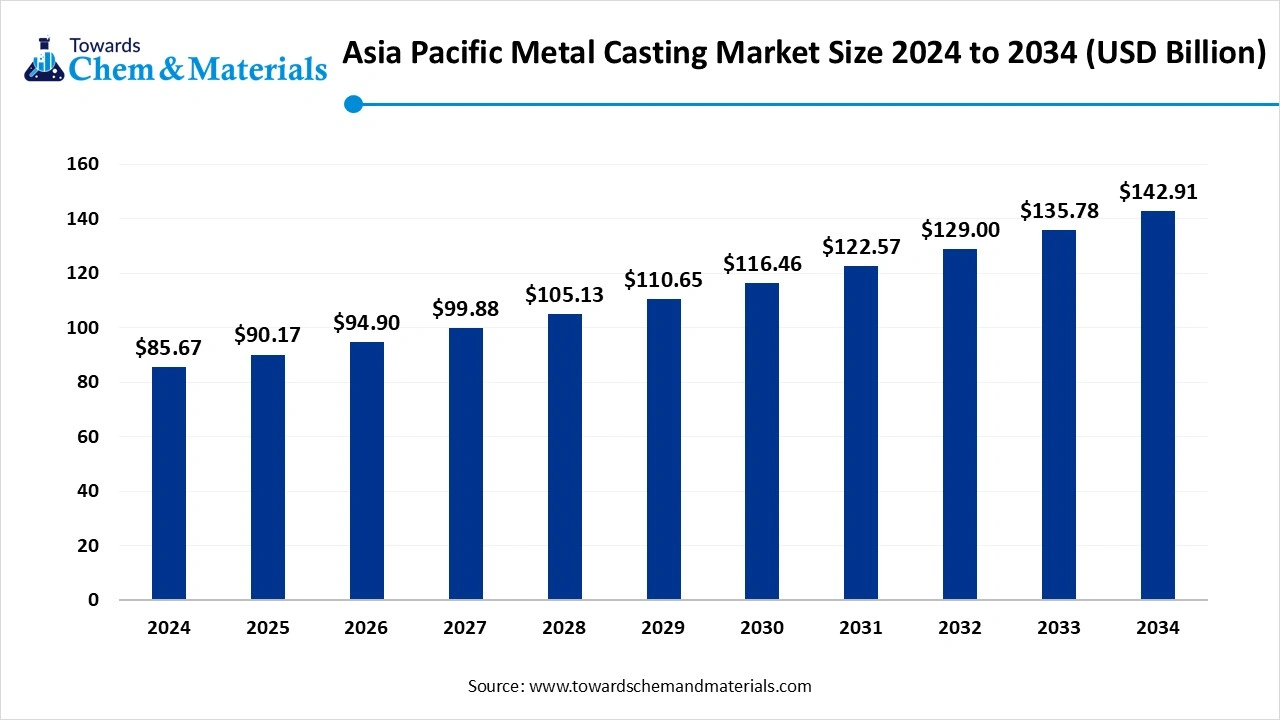

The Asia Pacific metal casting market size was reached at USD 96.85 billion in 2025 and is expected to be worth around USD 200.54 billion by 2035, growing at a compound annual growth rate (CAGR) of 7.55% over the forecast period 2025 to 2034.The ongoing urbanization and infrastructure development projects across the globe are the key factors driving market growth. Also, increasing emphasis on sustainability, coupled with the expanding automotive sector, can fuel market growth further.

Key Takeaways

- By country, China dominated the market by holding a 55% Asia Pacific metal casting market share in 2024. The dominance of the country can be attributed to the rising demand for industrial machinery and ongoing infrastructure development.

- By country, India is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the expanding automotive industry, rapid infrastructure development, and industrialization.

- By process, the sand-casting segment dominated the market with a 38% share in 2024. The dominance of the segment can be attributed to the rapid industrialization and infrastructure development.

- By process, the die casting segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the innovations in manufacturing technologies.

- By material, the cast iron segment led the market by holding 40% of market share in 2024. The dominance of the segment can be linked to the growing product demand from construction, automotive, and industrial machinery sectors.

- By material, the aluminum segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be driven by the region's robust manufacturing base.

- By application, the automotive segment held a 50% market share in 2024. The dominance of the segment is due to the surge in vehicle production and rapid infrastructure development in the region.

- By application, the aerospace & energy segment is expected to grow at the fastest CAGR during the projected period. The growth of the segment is owing to the increasing demand for durable and high-quality components.

- By end user, the automotive & transportation segment dominated the market with 48% market share in 2024. The dominance of the segment can be attributed to the rising need for lightweight vehicles.

- By end user, the energy & utilities segment is expected to grow at the fastest CAGR over the study period. The growth of the segment can be credited to the rising energy demand and ongoing investments in renewable energy sources.

- By distribution channel, the OEMs segment holds a 67% market share in 2024. The dominance of the segment can be linked to the surge in demand for electric vehicles (EVs) and government policies supporting domestic manufacturing.

- By distribution channel, the export/international supply segment is expected to grow at the fastest CAGR during the forecast period. The growth of the segment can be driven by rapid industrialization and infrastructure development.

Technological Advancements are Expanding Market Growth

Asia Pacific metal casting market covers the manufacturing and distribution of cast metal components produced through processes such as sand casting, die casting, investment casting, and gravity casting. Casting involves pouring molten metal into molds to form complex parts used in automotive, aerospace, construction, machinery, shipbuilding, energy, and consumer goods industries.

The market is driven by rapid industrialization in China, India, and Southeast Asia, expansion of automotive & electric vehicle production, infrastructure development, and demand for lightweight & precision-engineered components. Governments across APAC are promoting domestic manufacturing under initiatives like "Make in India" and "Made in China 2025," while private industries increasingly adopt advanced casting technologies for efficiency and cost reduction.

What Are the Key Trends Influencing the Asia Pacific Metal Casting Market?

- There is an increasing trend towards utilising cutting-edge alloys and composites in the metal casting sector. These materials provide robust durability, enhance strength and resistance to wear and corrosion, tailored to high demand uses in various sectors.

- The growing focus on lightweight components is another trend shaping a positive market trajectory. Sectors such as aerospace and automotive are increasingly prioritizing the production of lightweight components to enhance fuel performance and efficiency. The market is rapidly adapting to these demands by developing solutions for manufacturing lightweight parts.

- Many companies are heavily investing in R&D to innovate in metal casting materials and technologies. This investment is propelling innovation and helping major players to stay competitive in a rapidly complex and evolving market, leading to further market expansion.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 104.16 Billion |

| Expected Size by 2035 | USD 200.54 Billion |

| Growth Rate from 2025 to 2035 | CAGR 7.55% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Process, By Material, By Application, By End-User Industry, By Distribution Channel, By Country / Sub-Region, |

| Key Companies Profiled | Nemak, S.A.B. de C.V, Ryobi Limited, Ahresty Corporation, Aisin Corporation, Rheinmetall AG, Endurance Technologies Ltd., Kobe Steel, Ltd., Alcoa Corporation, Form Technologies, Inc., Linamar Corporation, Buhler AG, ArcelorMittal S.A. |

Market Opportunity

Increasing Adoption of X-ray Casting

The market is experiencing an increasing demand for innovative defect recognition technologies, like assisted defect recognition (ADR), which is a major factor creating lucrative opportunities in the market. Furthermore, X-ray technology's rapid evolution, with improvements in software or tubes integrating sophisticated algorithms, boosts this trend. Inline systems are widely used in manufacturing processes.

- In May 2025, the Indian government introduced a portal for recycling non-ferrous metals, such as lead, zinc, copper, and aluminium. The program was held in Delhi. This launch aims to improve the sustainability and minimize dependence on imported raw materials.(Source: www.alcircle.com)

Market Challenge

Regulatory Hurdles

Navigating evolving and complex regulatory frameworks can be hard for infrastructure projects, which is a major factor hindering market growth. The industry requires multiple approvals and permits across different levels, which leads to increased costs. Moreover, the constant fluctuations in the availability of raw materials affect the overall production efficiency and profitability.

Country Insight

China Asia Pacific Metal Casting Market Trends

China dominated the market by holding a 55% share in 2024. The dominance of the country can be attributed to the rising demand for industrial machinery and ongoing infrastructure development. Also, China is a major hub for automotive production. Metal casting is necessary for engine parts and chassis components. China's "New Infrastructure" strategy is driving the growth of the country's market further.

India Asia Pacific Metal Casting Market Trends

India is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the expanding automotive industry, rapid infrastructure development, and industrialization. In addition, Government initiatives such as "Make in India" are impelling domestic production, like metal casting, leading to market growth shortly.

Segmental Insight

Process Insights

Which Process Type Segment Dominated the Asia Pacific Metal Casting Market in 2024?

The sand-casting segment dominated the market with a 38% share in 2024. The dominance of the segment can be attributed to the rapid industrialization, infrastructure development, and the cost-effectiveness of sand casting processes. Also, the wide availability of high-quality foundry resources in countries such as China, India, and Japan is expected to impact positive segment growth shortly.

The die casting segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the innovations in manufacturing technologies and rapid industrialization across the globe. Moreover, the strong presence of various die casting manufacturers in the region and the availability of skilled labor are contributing to segment expansion further.

Material Insight

Why Cast Iron Segment Dominated the Asia Pacific Metal Casting Market in 2024?

The cast iron segment led the market by holding 40% market share in 2024. The dominance of the segment can be linked to the growing product demand from construction, automotive, and industrial machinery sectors. The growing demand for industrial machinery across different sectors, such as manufacturing and processing, is boosting the demand for cast iron components such as bearing housings and machine frames.

The aluminum segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be driven by the region's robust manufacturing base and rising demand for lightweight materials in the automotive sector. Aluminum's recyclability is a major factor, especially in the building and construction sector, because owners are opting for deconstruction over demolition.

Application Insight

How Much Share Did the Automotive Segment Held in 2024?

The automotive segment held a 50% market share in 2024. The dominance of the segment is due to the surge in vehicle production and rapid infrastructure development in the region. Additionally, government incentives such as tax cuts and subsidies are optimising investment in the automotive sector and related industries. China's rapid adoption of European automotive safety standards is further impeding positive segment growth.

The aerospace & energy segment is expected to grow at the fastest CAGR during the projected period. The growth of the segment is owing to the increasing demand for durable and high-quality components coupled with the technological advancements in casting processes. Furthermore, the use of innovative technologies such as 3D printing and investment in this sector will fuel segment growth soon.

End-User Insight

Which End-User Segment Dominated Asia Pacific Metal Casting Market in 2024?

The automotive & transportation segment dominated the market with 48% share in 2024. The dominance of the segment can be attributed to the rising need for lightweight vehicles, rapid innovations in casting technologies, and the ongoing expansion of the electric vehicle (EV) market. Also, the region's well-established automotive sector and supportive government policies lead to further segment growth.

The energy & utilities segment is expected to grow at the fastest CAGR over the study period. The growth of the segment can be credited to the rising energy demand and ongoing investments in renewable energy sources. The rapid modernization of power grids and the construction of new energy plants are also driving the growth of these segments over the forecast period.

Distribution Channel Insight

Why Did the Distribution Channel segment Held the Largest Asia Pacific Metal Casting Market Share in 2024?

The OEMs segment held a 67% market share in 2024. The dominance of the segment can be linked to the surge in demand for electric vehicles (EVs) and government policies supporting domestic manufacturing. Furthermore, innovations in energy-efficient casting methods and the utilisation of recycled materials are also contributing to the sector's sustainability goals.

The export/international supply segment is expected to grow at the fastest CAGR during the forecast period. The growth of the segment can be driven by rapid industrialization and infrastructure development, especially in nations such as China and India. Moreover, the region's other advantages, like cost-effectiveness and skilled labor, further boost its position in the market.

Asia Pacific Metal Casting Market-Value Chain Analysis

- Feedstock Procurement : It is the process of getting the raw materials utilized in the metal casting process. Feedstock procurement has a wider range of implications for cost efficiency, management, and sustainability within the industry.

- Chemical Synthesis and Processing : Chemical synthesis and processing play a crucial role in the market, impacting he efficiency, quality, and properties of cast products. Chemicals such as acids are utilized for cleaning, etching, and preparing metal surfaces before any other process.

- Packaging and Labelling : The packaging and labelling segment in the market underlines the importance of both the informational identification and physical protection of cast metal products.

- Regulatory Compliance and Safety Monitoring : Regulatory compliance and safety monitoring play an important role in the market, particularly given the hazardous nature of the processes involved and the rise in environmental scrutiny.

Recent Developments

- In April 2025, Automotive supplier Handtmann announced the manufacturing of new components for vehicle production utilizing the aluminum die casting process. Handtmann substantially minimizes the overall production time in automotive manufacturing and enhances material efficiency.(Source: www.foundry-planet.com)

Asia Pacific Metal Casting Market Top Companies

- Nemak, S.A.B. de C.V

- Ryobi Limited

- Ahresty Corporation

- Aisin Corporation

- Rheinmetall AG

- Endurance Technologies Ltd.

- Kobe Steel, Ltd.

- Alcoa Corporation

- Form Technologies, Inc.

- Linamar Corporation

- Buhler AG

- ArcelorMittal S.A.

Segments Covered

By Process

- Sand Casting

- Die Casting (High Pressure, Low Pressure)

- Investment Casting (Lost Wax)

- Gravity Casting

- Others (Centrifugal, Permanent Mold, 3D Sand Printing)

By Material

- Cast Iron (Gray Iron, Ductile Iron)

- Aluminum

- Steel

- Zinc

- Magnesium

- Others (Copper Alloys, Nickel Alloys, Titanium)

By Application

- Automotive (engines, chassis, wheels, transmission)

- Aerospace & Defense

- Construction & Infrastructure (pipes, fittings, structural components)

- Industrial Machinery & Equipment

- Shipbuilding & Marine

- Energy & Power (turbines, wind energy components)

- Consumer Goods & Electronics

By End-User Industry

- Automotive & Transportation

- Industrial & Heavy Machinery

- Construction & Infrastructure

- Aerospace & Defense

- Energy & Utilities

- Consumer & Electronics

By Distribution Channel

- OEMs (Original Equipment Manufacturers)

- Aftermarket & Spare Parts

- Export/International Supply

By Country / Sub-Region

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN (Indonesia, Thailand, Vietnam, Malaysia, Philippines, etc.)

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (2)