Content

Fire Stopping Materials Market Size, Share, Trends and Forecast Analysis

The global fire stopping materials market was valued at USD 3.85 billion in 2025, is estimated to reach USD 4.18 billion in 2026, and is projected to reach USD 8.83 billion by 2035, growing at a CAGR of 8.65% from 2026 to 2035. In terms of volume, the fire stopping materials market is projected to grow from 1.95 million tons in 2025 to 4.19 million tons by 2035. growing at a CAGR of 7.95% from 2026 to 2035.

Key Takeaways

- By region, Asia Pacific dominated the market with a share of 32% in 2025 and is expected to sustain its position while growing with the fastest CAGR of 10.2% in the forecast period. Rapid urbanization increases construction projects.

- By region, North America held the second largest share of 29% in 2025. Strict fire safety codes drive demand. Renovation activities boost market growth.

- By product type, the sealants segment dominated the market with 32% share in 2025. Increasing use in penetration sealing drives demand.

- By product type, the coatings segment held the second largest share of 24% in 2025 and is expected to have the fastest growth with a CAGR of 9.1% in the forecast period. Demand for passive fire protection in steel structures rises.

- By material type, the intumescent materials segment dominated the market with 36% share in 2025 and is expected to have the fastest growth with a CAGR of 9.3% in the forecast period. Expanding infrastructure projects increase demand.

- By material type, the cementitious materials segment held the second largest share of 23% in 2025. Cost-effective solutions drive adoption in developing markets

- By end-use industry, the construction segment dominated the market with 46% share in 2025. Urbanization increases building projects globally

- By end-use industry, the transportation segment held 10% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.9% in the forecast period. Railway and aviation infrastructure expand rapidly.

- By sales channel, the direct sales segment dominated the market with 48% share in 2025. Large projects prefer direct procurement.

- By sales channel, the online sales segment held the third largest share of 15% in 2025 and is expected to have the fastest growth with a CAGR of 10.1% in the forecast period. Wide network improves product availability.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 3.85 Billion | CAGR (2026–2035): 8.65%

- Market Projected Size (2035): USD 8.83 Billion

- Market Volume (2025): 1.95 Million Tons (MT) | Volume CAGR (2026–2035): 7.95%

- Market Projected Volume (2035): 4.19 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 2,160 per ton

- Average Selling Price: USD 3,070 per ton

- Pricing CAGR (2025–2035): 3.25%

Market Overview

What Is the Significance of the Fire Stopping Materials Market?

The fire stopping materials market is vital for enhancing building safety by sealing openings to prevent the spread of fire, smoke, and toxic gases. It is driven by strict building regulations, rapid urbanization, and increased demand in high-risk industrial sectors, ensuring safety and structural integrity. Stringent building codes and fire safety regulations mandate the use of these materials, making them essential for compliance in new construction and renovations.

Market Growth Trends:

- Sustainable and Advanced Materials: There is a strong move towards low-VOC, halogen-free, and environmentally friendly fire-stop materials, alongside innovations in intumescent and ablative technologies.

- Commercial and Industrial Growth: The commercial segment, including office spaces, malls, and data centers, dominates, while industrial facilities show high demand due to risks of operational downtime.

- Technological Integration: Digital construction tools, such as Building Information Modeling (BIM), are increasingly used for accurate specification and integration of fire-stopping into project planning.

Report Scope

| Report Attribute | Details |

| Market Volume in 2026 | USD 4.18 Billion / 2.11 Million Tons |

| Expected Volume by 2035 | USD 8.83 Billion / 4.19 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 8.65% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Material Type, By Application, By End-Use Industry, By Sales Channel, By Regions |

| Key Companies Profiled | RECTORSEAL CORPORATION, Sika AG, Specified Technologies, Inc, Etex Group, Morgan Advanced Materials, Knauf Insulation, RPM International Inc. |

Key Technological Shifts in The Fire Stopping Materials Market:

The fire stopping materials market is undergoing a rapid, technology-driven transformation, shifting from purely reactive, manual sealing methods to intelligent, sustainable, and high-performance engineered systems. Driven by stricter regulations like, IBC, NFPA and the growth of high-rise and complex infrastructure. Modern intumescent materials are engineered to expand faster and at lower temperatures, providing rapid containment before fire spreads.

Trade Analysis of Fire Stopping Materials Market: Import & Export Statistics

- According to Global Export Data, the world exported 1,295 Fire Protection System shipments between June 2024 to May 2025 (TTM) via 299 verified exporters and 258 buyers, representing a 25% YoY change.

- The Mexico, Vietnam, and the India lead as the top Fire Protection System importers, while United States with 1,010 shipments, China with 530 shipments, and Vietnam with 465 shipments ranks as the largest global Fire Protection System exporters.

Top-performing Global Fire Protection System Exporters by volume

- PIVA INTERNATIONAL DISTRIBUTION LLC: 54 shipments (15%)

- MINIMAX TECHNOLOGIES GMBH: 48 shipments (14%)

- TYCO FIRE PRODUCTS LP: 41 shipments (12%)

Supply Chain Analysis of Fire Stopping Materials Market

Material Production & Formulation

Fire stopping materials are produced through formulation of sealants, intumescent coatings, fire-resistant mortars, and barriers designed to prevent the spread of fire, smoke, and toxic gases through openings in buildings.

- Key players: 3M, Hilti, Rockwool International, Sika

Quality Testing and Certification

Fire stopping materials must meet stringent fire resistance, smoke control, and building safety standards before use in construction projects.

- Key players: Underwriters Laboratories, ASTM International, International Organization for Standardization, National Fire Protection Association

Distribution to Industrial Users

Fire stopping materials are supplied to construction companies, infrastructure developers, commercial building projects, industrial facilities, and residential housing sectors.

- Key players: 3M, Hilti, Sika.

Fire Stopping Materials Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| U.S. | National Fire Protection Association (NFPA); Occupational Safety and Health Administration (OSHA); International Code Council (ICC) | NFPA Fire Codes (e.g., NFPA 101, NFPA 5000); International Building Code (IBC); OSHA Safety Standards | Fire resistance, building safety compliance, installation standards | Fire stopping materials must meet fire-resistance ratings and be tested according to ASTM standards; compliance with building and fire codes is mandatory for construction projects. |

| Europe | European Commission; European Committee for Standardization (CEN) | Construction Products Regulation (CPR); EN Fire Resistance Standards (e.g., EN 1366) | Fire safety testing, product certification, CE marking | Fire stopping products must undergo fire resistance testing and obtain CE marking before being used in construction across the EU. |

| China | Ministry of Emergency Management (MEM); Ministry of Housing and Urban-Rural Development (MOHURD) | Fire Protection Law; Building Fire Codes | Fire safety compliance, construction standards | China enforces strict fire safety standards in buildings, driving demand for certified fire stopping materials. |

| India | Bureau of Indian Standards (BIS); National Building Code (NBC) authorities | National Building Code (NBC); Fire Safety Standards | Fire resistance, building safety, material testing | Fire stopping materials must comply with NBC fire safety requirements and BIS standards for use in infrastructure and commercial buildings. |

| Japan | Ministry of Land, Infrastructure, Transport and Tourism (MLIT) | Building Standards Act; Fire Service Act | Fire safety, construction compliance | Japan enforces strict fire-resistance standards for construction materials, including fire stopping systems. |

| Australia | Australian Building Codes Board (ABCB) | National Construction Code (NCC); Fire Resistance Level (FRL) standards | Fire resistance, building compliance | Australia mandates stringent fire performance testing and certification for fire stopping materials used in buildings. |

Segmental Insights

Product Type Insights

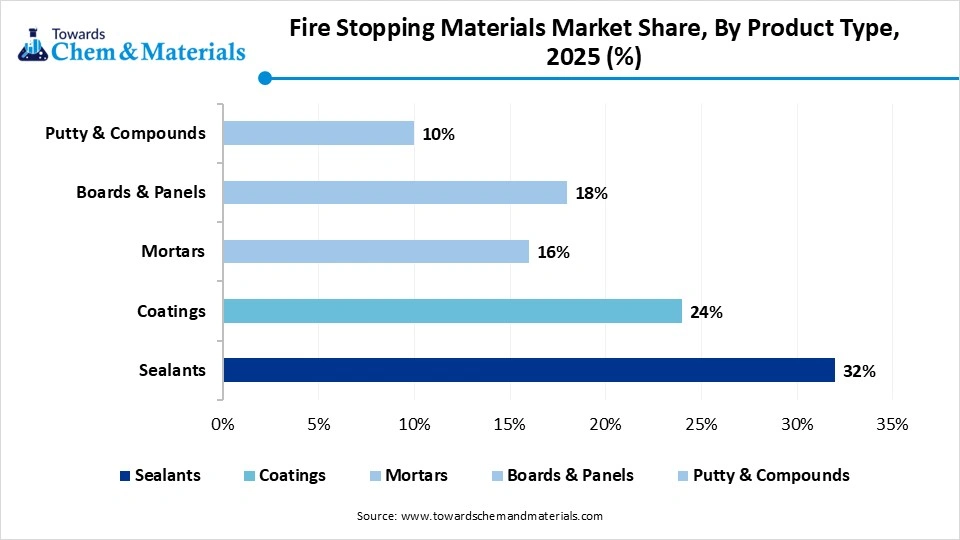

The Sealants Segment Dominated the Market with 32% Market Share in 2025

The sealants segment dominated the market with 32% share in 2025, driven by its leading role in sealing linear joints, cable penetrations, and curtain walls in high-rise and industrial constructions. Global enforcement of stricter fire safety codes requires passive fire protection, boosting demand for effective sealant products. Growth is fueled by advancements in intumescent sealants that expand under heat and elastomeric sealants that accommodate building movement.

The coatings segment held the second largest share of 24% in 2025 and is expected to have the fastest growth with a CAGR of 9.1% in the forecast period, driven by rising demand for structural steel protection in high-rise and industrial constructions, alongside stringent safety regulations. Advancements in intumescent technology, offering up to four hours of protection, and adoption of eco-friendly coatings are fueling this expansion. Rapid urbanization and the surge in commercial/industrial construction, have increased the consumption of fire-resistant coatings.

The boards and panels segment held the third largest share of 18% in 2025, driven by rising demand for high-performance, fire-rated construction in commercial, industrial, and high-rise residential buildings. This growth is propelled by stringent global safety codes, increasing infrastructure development, and the need for durable, efficient, and versatile fire protection solutions. Manufacturers are developing advanced fire-resistant particleboards and mineral-based panels that offer improved durability.

The mortars segment held the fourth largest share of 16% in 2025, due to surging demand for high-performance, durable fire-stopping in large-scale infrastructure projects, high-rise buildings, and industrial facilities. mortars are specifically designed for sealing large cable/pipe openings in high-risk areas like data centers, hospitals, and high-rise commercial structures. The rapid expansion of these sectors necessitates robust sealing solutions.

Fire Stopping Materials Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Sealants | 32% |

| Coatings | 24% |

| Mortars | 16% |

| Boards & Panels | 18% |

| Putty & Compounds | 10% |

Material Type Insights

The Intumescent Materials Segment Dominated the Market with 36% Market Share in 2025.

The intumescent materials segment dominated the market with 36% share in 2025 and is expected to have the fastest growth with a CAGR of 9.3% in the forecast period, due to rising demand for high-performance passive fire protection, stringent fire safety regulations, and rapid infrastructure urbanization. These materials are preferred for their ability to expand under high temperatures, providing crucial insulation for structural steel, cable penetrations, and joints in modern, high-rise buildings.

The cementitious materials segment held the second largest share of 23% in 2025, due to its superior durability, high fire resistance, and cost-efficiency in structural steel protection. As part of the broader passive fire protection industry expected to grow rapidly these materials are increasingly utilized in high-rise, commercial, and industrial infrastructure projects to meet stringent safety codes.

The silicone materials segment held the third largest share of 19% in 2025, driven by rising demand for high-performance sealants in modern construction. Silicone offers superior flexibility, durability, and fire resistance, making it ideal for sealing high-rise buildings and infrastructure against fire, smoke, and toxic gas spread. Enhanced building codes globally are mandating superior fire protection materials, boosting the demand for advanced silicone-based firestop solutions.

The elastomeric materials segment held the fourth largest share of 12% in 2025, due to their high flexibility, durability, and superior sealing capabilities against smoke and fire in modern construction. Growing safety regulations and the need to protect against both fire and toxic smoke in commercial and residential applications are major drivers. These materials are highly valued for their ability to maintain the integrity of fire-rated walls and floors in infrastructure projects, supporting the overall market growth.

Fire Stopping Materials Market Share, By Material Type, 2025 (%)

| By Material Type | Revenue Share, 2025 (%) |

| Intumescent Materials | 36% |

| Cementitious Materials | 23% |

| Silicone Materials | 19% |

| Elastomeric Materials | 12% |

| Mineral Wool | 10% |

End-Use Industry Insights

The Construction Segment Dominated the Market with 46% Market Share in 2025

The construction segment dominated the market with 46% share in 2025, driven by booming construction activities and stringent, globally adopted safety regulations. Increasing enforcement of building codes demands fire-rated passive protection to prevent smoke and fire spread in new and retrofitted buildings. increased investment in complex infrastructure, further supports growth.

The manufacturing segment held the second largest share of 18% in 2025 driven by rapid industrial expansion, stricter global safety codes, and the need for high-performance sealants in critical infrastructure. Manufacturers are developing advanced intumescent materials that expand upon exposure to heat, providing superior protection. Industrial sectors are increasing adoption to prevent operational downtime from fire hazards.

The oil and gas segment held the third largest share of 14% in 2025, due to intensified safety regulations in refineries and high-risk, large-scale infrastructure projects. Rapid expansion of oil and gas infrastructure, including pipelines and storage facilities, requires heavy investment in passive fire protection systems. Increasing reliance on advanced sealant and passive fire protection systems to comply with stringent fire safety regulations in petrochemical plants is driving demand.

The energy and power segment held the fourth largest share of 12% in 2025, driven by the expansion of critical electrical infrastructure, renewable energy projects, and stringent safety regulations. Rising demand for high-performance sealants and passive fire protection is fueled by the need to secure electrical penetrations in data centers, power plants, and utility substations to prevent fire and smoke spread.

The transportation segment held 10% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.9% in the forecast period, due to massive investments in transit infrastructure like airports, metro systems and strict safety regulations requiring fire-rated sealing for high-occupancy structures. This growth is fueled by increasing needs to protect complex, multi-penetration infrastructure against fire, smoke, and toxic gas spread.

Sales Channel Insights

The Direct Sales Segment Dominated the Market with 48% Market Share in 2025

The direct sales segment dominated the market with 48% share in 2025, by leveraging specialized technical support, direct-to-contractor partnerships, and the need for certified installation expertise in high-rise and industrial construction. This approach addresses rising demand for, and strict compliance with, passive fire safety regulations. Stricter enforcement of fire safety norms by regulatory bodies in 2025 requires advanced, certified passive fire protection materials.

The distributors segment held the second largest share of 37% in 2025, driven by the need for localized, rapid supply chains to support surging construction, urbanization, and strict fire safety regulations. Distributors are vital for navigating supply chain fragilities, such as increased logistical costs, and ensuring timely delivery of materials to project sites, with sealant demand particularly high.

The online sales segment held the third largest share of 15% in 2025 and is expected to have the fastest growth with a CAGR of 10.1% in the forecast period, due to the digitization of construction procurement, providing contractors and DIY users with direct access to specialized products like sealants and putties. This shift is accelerated by the need for quick, on-demand sourcing of fire-rated materials, offering easier product comparison, fast delivery, and access to technical documentation.

Fire Stopping Materials Market Share, By Sales Channel, 2025 (%)

| By Sales Channel | Revenue Share, 2025 (%) |

| Direct Sales | 48% |

| Distributors | 37% |

| Online Sales | 15% |

Regional Insights

How did Asia Pacific Dominate the Fire Stopping Materials Market in 2025?

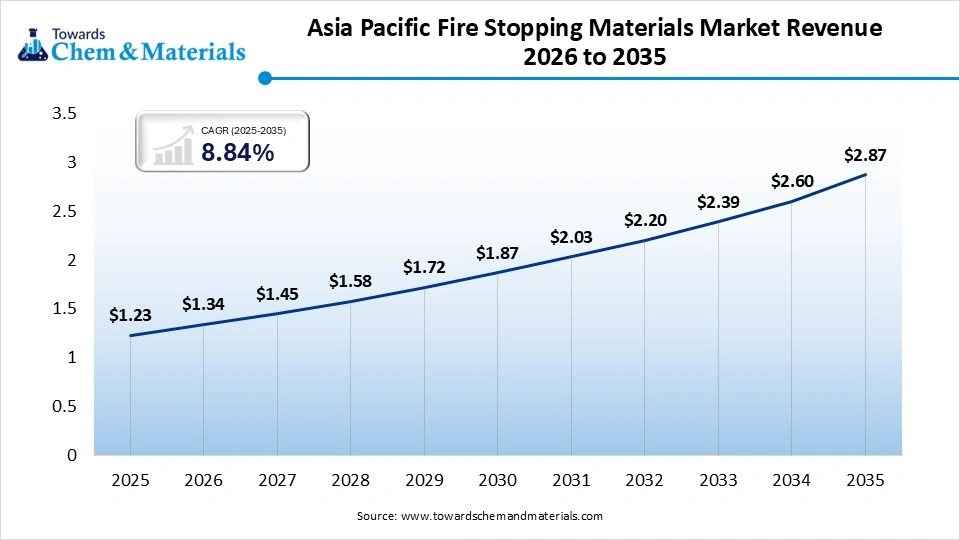

The Asia Pacific fire stopping materials market size was estimated at USD 1.23 billion in 2025 and is projected to reach USD 2.87 billion by 2035, growing at a CAGR of 8.84% from 2026 to 2035. The market is experiencing high growth due to increased infrastructure investment in China, India, and Southeast Asia. Governments are enforcing mandatory fire safety regulations to reduce accidents, increasing the adoption of passive fire protection systems. The construction industry’s rapid development is boosted by rising disposable incomes, urbanization, and industrialization.

India Fire Stopping Materials Market Growth Factor

The fire stopping materials market in India is experiencing rapid growth, driven by stringent National Building Code (NBC) regulations and surging high-rise commercial/residential construction, the market is shifting toward advanced, high-performance passive fire protection systems, with significant demand in electrical applications. Strict enforcement of fire safety norms in construction, particularly in urban areas, is mandating the use of fire-stopping sealants, coatings, and boards.

North America Fire Stopping Materials Market Growth Factor

North America held the second largest share of 29% in 2025, the growth of the market in the region is driven by the strict fire safety codes which drives the demand for the market. the advanced construction practices also support the adoption due to growing infrastructure development and need for safety awareness further supports growth of the market. the renovation activities also further boost the market growth and expansion.

U.S. Fire Stopping Materials Market Growth Factor

The U.S. fire stopping materials market is experiencing strong growth, driven by stringent building codes (IBC/NFPA), rising urbanization, and increased demand for passive fire protection in residential and commercial sectors. Intense focus on fire safety, particularly in California and other regions prone to wildfires, has accelerated the adoption of advanced fire-resistant technologies. Continued investment in multi-family housing, mixed-use developments, and data centres drives demand for robust passive fire protection systems, fueling growth in the market.

Fire Stopping Materials Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 29% |

| Europe | 25% |

| Asia-Pacific | 32% |

| Latin America | 8% |

| Middle East & Africa | 6% |

Recent Developments

- In February 2026, PPG has launched PPG STEELGUARD 652, a water-based, UL 263-certified intumescent coating designed for interior structural steel that offers up to two hours of fire protection. The low-VOC product is available in North America and provides long-term durability for up to 20 years.

- in September 2025, AkzoNobel has launched Chartek ONE in Europe, an advanced epoxy passive fire protection solution designed for onshore and offshore energy infrastructure. The product offers improved application efficiency for protecting against hydrocarbon fires and cryogenic spills, meeting rising safety and sustainability standards in the region.

Top players in the Fire Stopping Materials Market & Their Offerings:

- Hilti Corporation: Hilti is a leading provider of passive fire protection systems, offering a comprehensive portfolio of firestop products including sealants, collars, wraps, and fire-resistant foams. The company focuses on integrated fire protection solutions for construction, infrastructure, and industrial applications.

- 3M Company: 3M provides advanced firestop materials such as sealants, putties, and fire barrier systems designed to prevent the spread of fire, smoke, and toxic gases. Its solutions are widely used in commercial buildings, healthcare facilities, and industrial environments.

- BASF SE: BASF supplies raw materials and additives used in fire stopping systems, including flame-retardant chemicals and high-performance polymers. The company focuses on developing sustainable and high-efficiency fire protection solutions.

- Sika AG: Sika offers a wide range of firestop sealants, coatings, and mortars used in construction and infrastructure projects. The company emphasizes durable, high-performance materials that comply with global fire safety standards.

Fire Stopping Materials Market Top Players

- RECTORSEAL CORPORATION

- Sika AG

- Specified Technologies, Inc

- Etex Group

- Morgan Advanced Materials

- Knauf Insulation

- RPM International Inc.

Fire Stopping Materials Market Segments Covered:

By Product Type

- Sealants

- Silicone-based Sealants

- Acrylic Sealants

- Intumescent Sealants

- Coatings

- Cementitious Coatings

- Intumescent Coatings

- Mortars

- Gypsum-based Mortars

- Cement-based Mortars

- Boards & Panels

- Calcium Silicate Boards

- Gypsum Boards

- Putty & Compounds

- Firestop Putty

- Firestop Compound

By Material Type

- Intumescent Materials

- Graphite-based

- Vermiculite-based

- Cementitious Materials

- Silicone Materials

- Elastomeric Materials

- Mineral Wool

By Application

- Electrical Penetrations

- Cable Trays

- Conduits

- Mechanical Penetrations

- Pipes

- Ducts

- Structural Joints

- Expansion Joints

- Curtain Wall Joints

- Openings & Voids

- Wall Openings

- Floor Openings

By End-Use Industry

- Construction

- Residential

- Commercial

- Industrial

- Oil & Gas

- Energy & Power

- Transportation

- Railways

- Aviation

- Manufacturing Facilities

By Sales Channel

- Direct Sales

- Distributors

- Online Sales

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)