Content

What is the Biodegradable Plastics Market Size and Share?

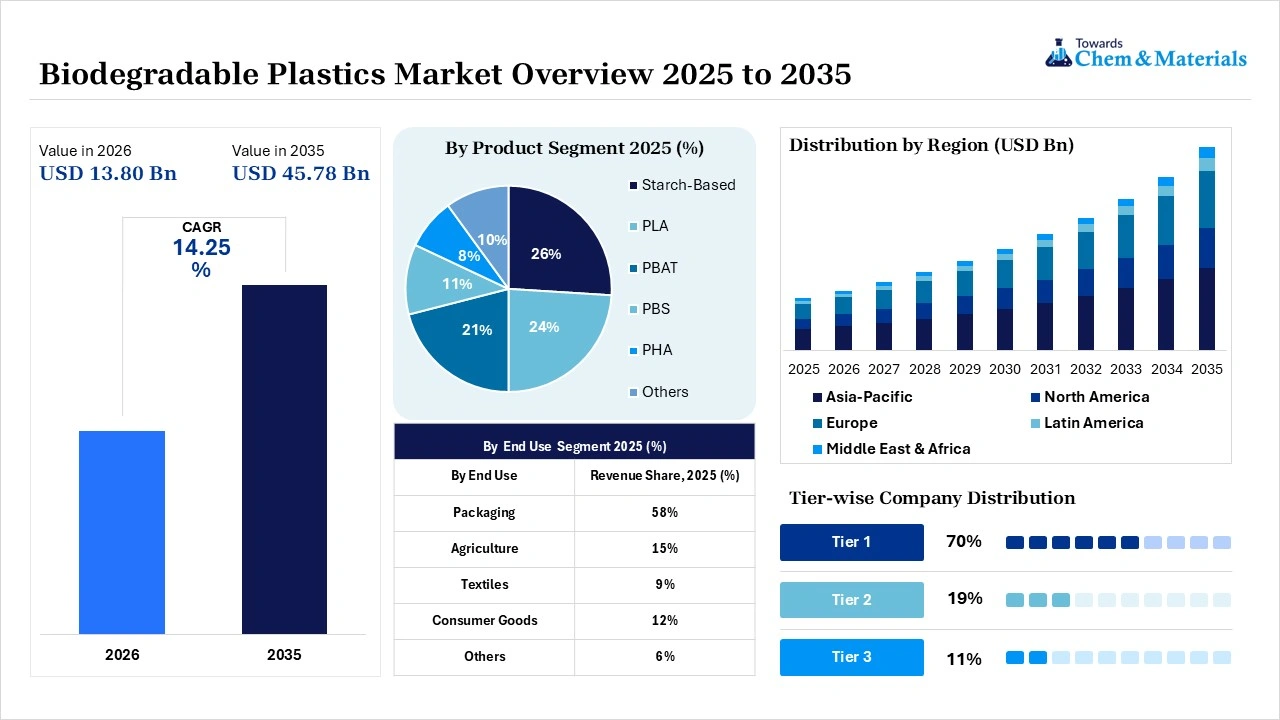

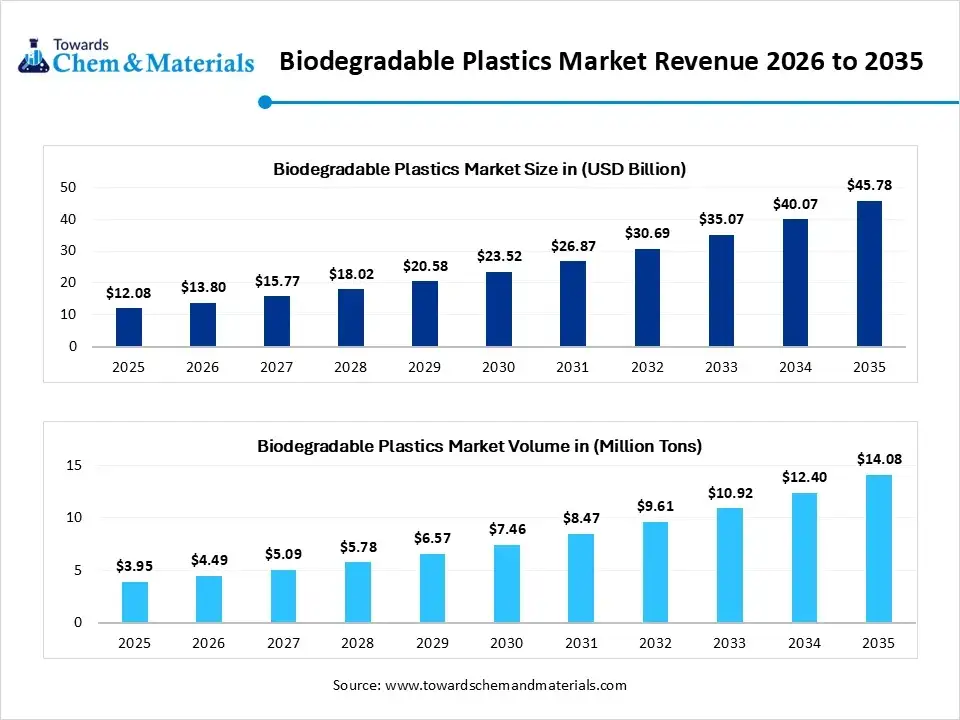

The biodegradable plastic market size was valued at USD 12.08 billion in 2025, is estimated to reach USD 13.80 billion in 2026, and is projected to reach USD 45.78 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 14.25% over the forecast period from 2026 to 2035.Asia Pacific dominated the biodegradable plastic market with the largest revenue share of 41% in 2025 and is expected to grow at the fastest CAGR of 14.40% during the forecast period. In terms of volume, the biodegradable plastic market is projected to grow from 3.95 million tons in 2025 to 14.08 million tons by 2035. growing at a CAGR of 13.55% from 2026 to 2035.Increasing corporate sustainability commitments is the key factor driving market growth. Also, increasing consumer demand for sustainable packaging coupled with the stringent government regulations can fuel market growth further. Moreover, the expansion in food delivery and e-commerce services has facilitated an extensive upsurge in the need for biodegradable materials.

Market Highlights

- By region, Asia Pacific dominated the market with the largest share of 41% in 2025. The dominance of the region can be attributed to a combination of strict regulatory bans on single-use plastics.

- By region, Europe held the market share of 28% in 2025 and is expected to grow at the fastest CAGR of 14.10% over the forecast period. The growth of the region can be credited to strict single-use plastic regulations.

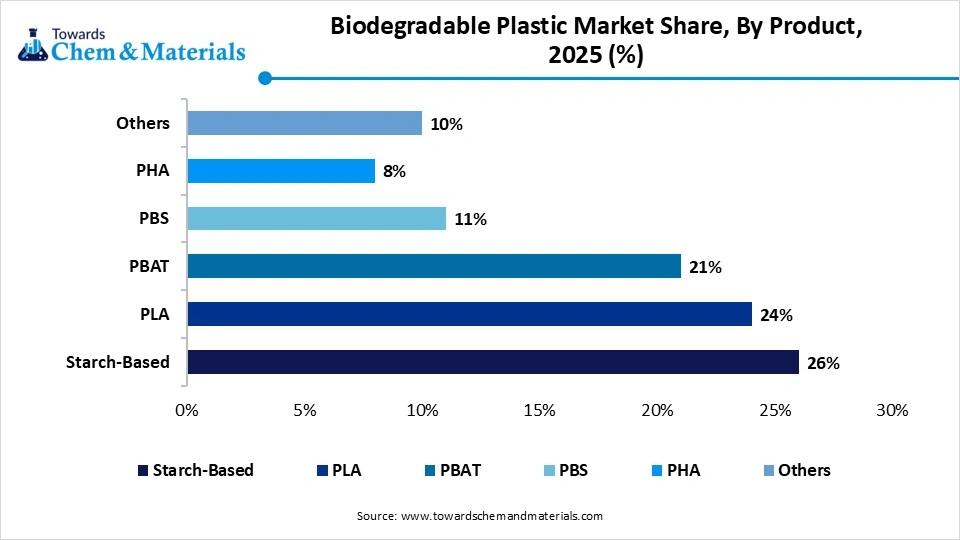

- By product, the starch-based segment dominated the market with the largest share of 26% in 2025. This segment is valued as a main alternative to petroleum-based resins and influenced by the ongoing scale-up of agricultural waste valorization.

- By product, the PBAT segment held the market share of 21% in 2025 and is expected to grow at the fastest CAGR of 14.5% over the forecast period. PBAT (Polybutylene Adipate Terephthalate) is fully biodegradable, flexible, and heavily utilized in agricultural films.

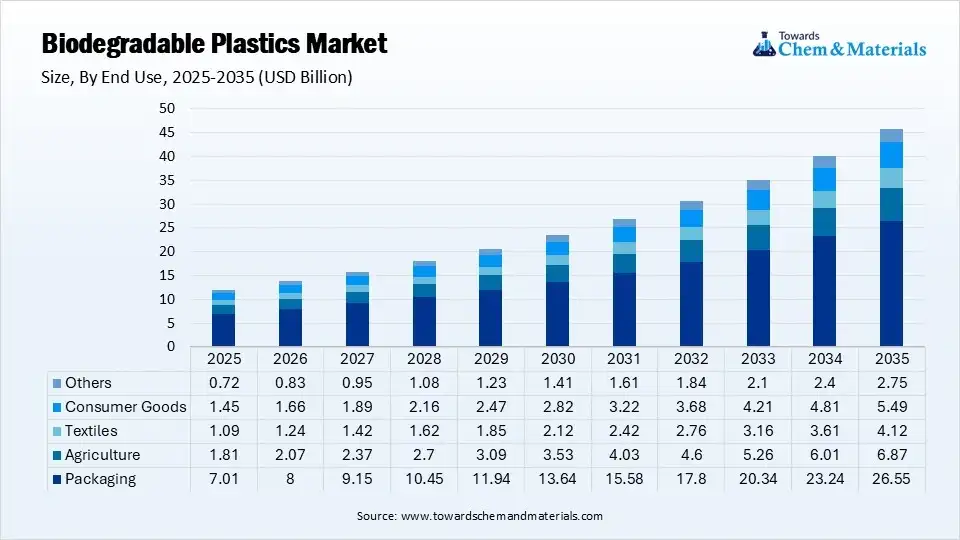

- By end use, the packaging segment dominated the market with the largest share of 58% in 2025. This segment includes wraps, shopping bags, pouches, and agricultural mulch films. Vegetable starch blends and polylactic acid (PLA) are integrated here to create high-volume single-use retail and takeaway bags.

- By end use, the others segment held the market share of 6% in 2025 and is expected to grow at the fastest CAGR of 13.9% during the projected period. The segment encompasses emerging and specialized areas outside of primary sectors such as agriculture and textiles.

Quick Stats at a Glance

- Market in Size 2025 : USD 12.08 Billion | CAGR (2026–2035): 14.25%

- Market Estimated Size in 2026: USD 13.80 Billion

- Market Projected Size by 2035: USD 45.78 Billion

- Asia Pacific: largest Regional Market Revenue Share of 41% in 2025 | USD 4.95 Billion

- Europe: Fastest-growing Regional Market Revenue Share of 28% in 2025 | USD 3.38 Billion

- Market Volume in 2025: 3.95 Million Tons | Volume CAGR (2026–2035): 13.55%

- Market Estimated Volume in 2026: 4.19 Million Tons

- Market Projected Volume by 2035: 14.08 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 2,770/Ton

- Average Selling Price (2025): USD 3,490/Ton

- Pricing CAGR (2026–2035): 2.85%

The growing need for sustainable packaging solutions is fueling the use of biodegradable plastics, especially in consumer goods and food and beverage sectors, where sustainable alternatives are becoming crucial. Market players are emphasizing more biopolymer innovations, like starch-based plastics and PLA/PHA, to replace conventional packaging materials, minimize overall plastic waste, and present vital opportunities in the market.

- For instance, Qore, a joint venture between Minnesota-based Cargill and Germany-based HELM, has officially commenced operations at its $300-million facility in Eddyville, Iowa. The plant will produce 66,000 metric tons annually of QIRA, the world's first large-scale 1,4-butanediol (BDO) derived from locally grown dent corn.(Source: www.businesswire.com)

The ongoing transition toward compostable packaging and bio-based materials in emerging economies such as the Asia Pacific is enabling consumers to focus on sustainable products and solutions.Common types of biodegradable plastics include polyhydroxyalkanoates (PHA), polylactic acid (PLA), and starch blends.

Global Investment Flow for Biodegradable Plastics 2026

The global investment flow for the market is mainly fueled by an extensive transition from niche venture funding to institutional and large-scale capital expenditures (CapEx). Fueled by corporate mandates to minimize Scope 3 emissions, capital allocation is focusing on industrial-scale capacity expansion over the forecast period.

- NatureWorks LLC has inaugurated a new polylactic acid (PLA) facility in Thailand, adding 75,000 metric tons of annual capacity. This strategic expansion enables the bioplastics manufacturer to better serve rapidly growing Asian markets while strengthening its global production footprint.(Source: www.plasticsnews.com)

Major venture and corporate capital focus on Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) scale-up facilities to replace fossil-based plastics.

Market Trends

- The increasing demand for sustainable farming practices and alternatives to conventional plastic materials is the latest trend in the market, shaping positive market growth. Also, the transition towards biodegradable plastics aligns well with global efforts to minimize the environmental impact of plastic waste and agricultural practices.

- The rising focus on sustainable health care solutions and materials is one of the major factors fueling market expansion in recent years. The rapid transition towards biocompatible and eco-friendly materials in the medical sector is propelling demand for biodegradable plastics to replace conventional petroleum-based plastics in medical devices.

- Ongoing innovations in biodegradable materials are the future trend in the market driving market growth. Innovations in material science have facilitated the development of new biodegradable polymers that give improved versatility and performance.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 13.80 Billion / 4.49 Million Tons |

| Revenue Forecast in 2035 | USD 45.78 Billion / 14.08 Million Tons |

| Growth Rate | CAGR 14.25% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Product, By End Use, By Region |

| Key Companies Profiled | BASF, NatureWorks LLC, TotalEnergies, Novamont S.p.A, FkuR (Germany), DuPont (U.S.), Biome Bioplastics (U.K.), Mitsubishi Chemical Group Corporation (Japan), TORAY INDUSTRIES, INC. (Japan), Dow (U.S.), Plantic (Australia), Hubei Tianan Hongtai Biotechnology Co., Ltd. (China), Danimer Scientific (U.S.), Evonik (Germany), Eastman Chemical Company (U.S.), DAIKIN INDUSTRIES, Ltd. (Japan), Solvay (Belgium) |

Supply Chain Analysis of the Biodegradable Plastic Market

- Production & Processing :It includes the methods of synthesizing biodegradable polymers from essential raw materials and converting them into finished products. These processes, mainly polymerization, fermentation, extrusion, and injection molding, are used to create agricultural films, compostable packaging, and medical devices to minimize landfill waste. These materials are either bio-based or synthesized from fossil-based resources.

- NatureWorks LLC: Based in the US, this joint venture is a major global supplier of PLA resins (branded as Ingeo) used in packaging and 3D printing.

- Other Key Players: Danimer Scientific, Novamont S.p.A.

- Quality Testing and Certification :It includes an important standard section emphasizing the technical verification, environmental standards, and compliance frameworks required to validate bioplastic products. Because traditional plastic can easily be mislabeled as "eco-friendly," this section dictates how materials are scientifically proven to break down safely without harming the ecosystem. It is also crucial for adhering to stringent environmental mandates, like bans on single-use plastic across Europe and Asia.

- BASF SE: Produces ecovio® and ecoflex®, which are heavily certified for industrial compostability and agricultural soil biodegradation.

- Other Key Players: Novamont S.p.A., Danimer Scientific

- Distribution to Industrial Users :It includes the supply chain channel where bioplastic resins are sold to large-scale market players rather than to consumers. These players convert the raw plastics into textiles, packaging, or agricultural goods. The major players dominating this specific node of the supply chain are divided into biopolymer manufacturers and specialized industrial distributors/compounders who facilitate localized delivery.

- Danimer Scientific: A U.S.-based company focused on the development of PHA (polyhydroxyalkanoates), which are highly biodegradable in various environments.

- Other Key Players: TotalEnergies, Corbion, and Mitsubishi Chemical Corporation.

Biodegradable Plastic Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union | Under Article 5, the EU bans specific items like cutlery and straws. Critically, this directive treats most chemical-modified biodegradable plastics (like PLA) the same as conventional plastics, meaning they cannot be used to bypass these bans unless certified otherwise. |

| United States | Greenwashing. It is illegal to label any consumer product as "biodegradable" or "degradable" unless it meets exact scientific certification standards like ASTM D6400 for industrial composting. Products must actively degrade without leaving toxic PFAS or synthetic chemical residues. |

| China | National Standard GB/T 41010-2021: Establishes definitive criteria for degradation performance and sets explicit labeling requirements for all degradable plastics sold within domestic sectors. |

| India | Producers of biodegradable or compostable alternative plastics cannot market their products without obtaining an official compliance certificate from the CPCB. |

Market Dynamics

Driver

Growing Environmental Awareness

The increasing awareness regarding environmental issues among the majority of consumers is the major factor driving market growth. Consumers are increasingly becoming aware of the conventional plastics' impact on ecosystems and human health. In addition, as both individuals and organizations increasingly prioritize sustainability, the biodegradable plastic market is poised for a surge in expansion. This growth is driven by a collective commitment to minimizing plastic waste and advancing environmentally responsible practices.

Restraint

Performance and Technical Limitations

Pure biopolymers such as starch-based plastics are brittle. Also, thermoplastic starch (TPS) modifications result in low mechanical strength, poor thermal stability, and high moisture sensitivity, which is the major hindrance to market growth. Moreover, to match the mechanical strength of petroleum-based plastics, manufacturers must synthesize biopolymers with external polyesters, such as PBAT or PCL, hence increasing production complexity further.

Opportunity

Shift Towards Greener Packaging

Extensive adoption of plastic bag bans shows crucial results in minimizing waste along coastlines, creating lucrative opportunities in the market. As traditional plastics face many restrictions, markets are exploring solutions that align with both regulatory standards and environmental goals. Furthermore, the packaging sector is undergoing rapid evolution, with biodegradable materials emerging as a viable strategy to reconcile operational efficacy with ecological stewardship. These shifts in market dynamics are evident as consumers increasingly prioritize products and practices that foster environmental sustainability.

Segmental Insights

Product Insights

The starch-based segment dominated the market with the largest share of 26% in 2025. This segment is valued as a main alternative to petroleum-based resins and influenced by the ongoing scale-up of agricultural waste valorization and stringent regulatory bans on single-use plastics. Raw starch is highly brittle and crystalline. To overcome moisture sensitivity, major players combine it with other biodegradable polyesters such as PBAT or PBS. In addition, modern starch-based compounds exhibit exceptional versatility and seamlessly integrate with standard processing equipment utilized for extrusion, injection molding, and blow molding. Generally used to produce single-use items like food delivery containers and straws.

")

The PBAT segment held the market share of 21% in 2025 and is expected to grow at the fastest CAGR of 14.5% over the forecast period. PBAT (Polybutylene Adipate Terephthalate) is a fully biodegradable, flexible, and heavily utilized material in agricultural films and flexible packaging. It possesses high tear strength, impact strength, and exceptional elongation. It behaves much like traditional low-density polyethylene (LDPE), making it ideal for film blowing.

Furthermore, polybutylene adipate terephthalate (PBAT) serves as a superior material for agricultural mulch films. Its biodegradability enables farmers to incorporate the organic sheets directly into the soil post-harvest, hence mitigating the accumulation of traditional plastic micro-waste. It's mostly used in single-use consumer products and organic waste bags, leading to segment growth soon.

Biodegradable Plastic Market Share,By Product, 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Starch-Based | 26% |

| PLA | 24% |

| PBAT | 21% |

| PBS | 11% |

| PHA | 8% |

| Others | 10% |

End Use Insights

The packaging segment dominated the market with the largest share of 58% in 2025. This segment includes wraps, shopping bags, pouches, and agricultural mulch films. Vegetable starch blends and polylactic acid (PLA) are integrated here to create high-volume single-use retail and takeaway bags. The ongoing expansion of food-delivery apps creates extensive demand for compost-ready formats. Also, major fast-food brands are converting to PLA-coated cups, cutlery, and salad containers to achieve corporate waste-diversion goals. The global expansion of e-commerce has expedited the integration of biodegradable protective mailers, bubble wraps, and loose-fill cushioning as sustainable alternatives to conventional polystyrene packaging materials, impacting positive segment growth soon.

")

The other segment held the market share of 6% in 2025 and was expected to grow at the fastest CAGR of 13.9% during the projected period. The segment encompasses emerging and specialized areas outside of primary sectors such as agriculture and textiles. It is heavily used in bioabsorbable and biocompatible implants, surgical sutures, drug delivery systems, and tissue engineering scaffolds. Moreover, it is incorporated into single-use articles, cosmetic packaging, and exfoliating scrubs; these materials are engineered to dissolve or degrade safely within aquatic ecosystems. The continuous evolution of advanced polymers, such as polyhydroxyalkanoates (PHA), engineered to endure fluctuating temperatures and mechanical stress, has significantly expanded their applicability in high-tech medical and automotive sectors.

Biodegradable Plastic Market Share,By End Use, 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| Packaging | 58% |

| Agriculture | 15% |

| Textiles | 9% |

| Consumer Goods | 12% |

| Others | 6% |

Regional Analysis

How did Asia Pacific Dominate the Biodegradable Plastic Market in 2025?

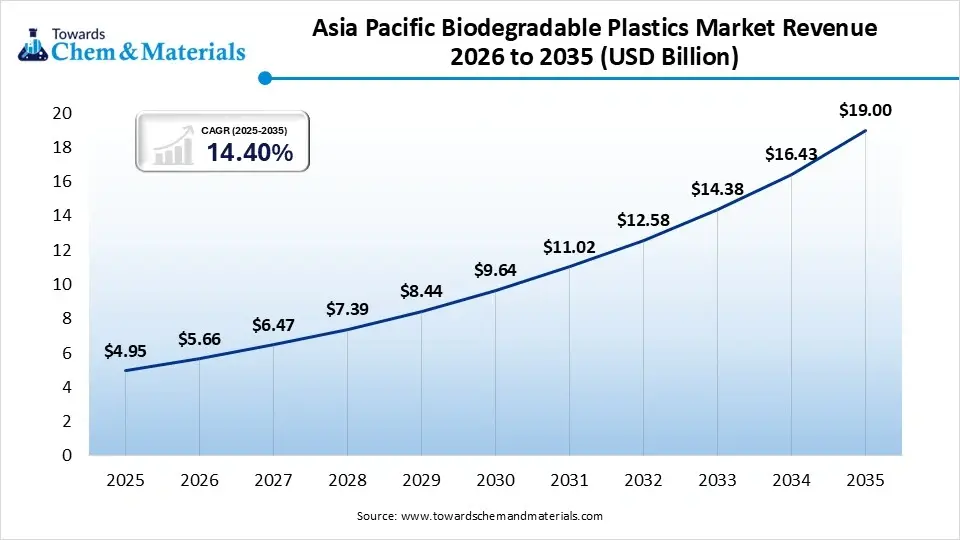

The Asia Pacific biodegradable plastic market size was estimated at USD 4.95 billion in 2025 and is projected to reach USD 19.00 billion by 2035, growing at a CAGR of 14.40% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 41% in 2025. The dominance of the region can be attributed to a combination of strict regulatory bans on single-use plastics and surging demand from the e-commerce and food delivery sectors, along with an abundant supply of agricultural feedstocks. In addition, this market shift is further propelled by corporate sustainability initiatives and heightened consumer awareness regarding plastic pollution and landfill waste.

China

- The National Development and Reform Commission (NDRC) has enforced aggressive phased bans on non-degradable single-use plastics and bags and delivery sectors to adopt sustainable alternatives.

- Increasing awareness of plastic pollution among Chinese consumers is driving a structural shift in retail purchasing, accelerating the adoption of bio-based solutions.

India

- Agriculture is rapidly adopting biodegradable mulch films, while research grants from organizations like the Indian Institute of Science (IISc) are pioneering newer, durable biopolymers.

- Shifting environmental awareness and a preference for "green" products force retailers and brands to package goods responsibly.

The Europe biodegradable plastic market size was estimated at USD 3.38 billion in 2025 and is projected to reach USD 13.05 billion by 2035, growing at a CAGR of 14.46% from 2026 to 2035.Europe held a market share of 28% in 2025 and was expected to grow at the fastest CAGR of 14.10% over the forecast period. The growth of the region can be credited to strict single-use plastic regulations, ambitious European Union waste reduction mandates, and heightened consumer sustainability awareness. Furthermore, European automotive manufacturers are increasingly adopting lightweight, UV-resistant bioplastics for electric vehicle production, while the agricultural sector utilizes biodegradable mulch films to mitigate soil contamination.

Germany

- China's implementation of stringent policies eliminating non-degradable single-use plastics and expanded polystyrene (EPS) packaging requires commercial entities to shift entirely to sustainable alternatives.

- The extensive use of delivery apps and e-commerce giants has forced a corporate shift toward biodegradable packaging.

France

- France has been at the forefront of enforcing bans on single-use plastics (such as plates, cups, and cotton buds) and aggressively pushing for a circular economy.

- French companies face mounting pressure and public scrutiny to eliminate traditional petroleum-based plastics, accelerating the adoption of bio-based and compostable alternatives.

The North America biodegradable plastic market size was estimated at USD 2.42 billion in 2025 and is projected to reach USD 9.38 billion by 2035, growing at a CAGR of 14.51% from 2026 to 2035.North America held a market share of 20% in 2025. The growth of the region can be linked to the growing local government bans on conventional, single-use petroleum plastics, compelling industries to source certified eco-friendly materials. Also, rapid volume expansion across the food, beverage, and personal care sectors is driving high demand for technically advanced, thin-film biodegradable barrier resins, leading to regional growth soon.

United States

- Consumers in the country are actively seeking "green" alternatives, pushing major consumer packaged goods (CPG) companies to replace petroleum-based plastics with plant-based options to satisfy brand loyalty.

- Investments by municipalities and private entities into organic recycling and large-scale industrial composting facilities are generating more reliable end-of-life pathways for biodegradable plastics.

Canada

- Aggressive federal mandates, such as the national ban on specific single-use plastic items, are forcing industries to transition to sustainable alternatives.

- An increasing public awareness of plastic pollution is driving everyday shoppers and retail sectors to actively seek out green, compostable products.

The Latin America biodegradable plastic market size was estimated at USD 0.72 billion in 2025 and is projected to reach USD 2.98 billion by 2035, growing at a CAGR of 15.26% from 2026 to 2035.Latin America held a market share of 6% in 2025. The growth of the region can be linked to the increasing consumer awareness, evolving regulatory frameworks, and extensive agricultural resources, with Brazil, Mexico, and Chile leading the market. Moreover, these advanced materials optimize crop yields and naturally decompose them in the soil, effectively mitigating agricultural waste disposal challenges.

")

Brazil

- Brazil's booming food processing and delivery sectors bring a massive push for bio-based, compostable packaging that fits corporate sustainability and circular economy goals.

- Major brands are increasingly transitioning to biodegradable polymers (PHA, PLA, and starch blends) to meet public sustainability expectations & ESG metrics.

Argentina

- Increasing regional regulations and municipal bans on single-use conventional plastics have forced manufacturers to pivot towards sustainable alternatives.

- Argentina’s massive agricultural sector (specifically corn and sugarcane) offers a highly accessible, low-cost supply of starches and cellulose.

The Middle East & Africa biodegradable plastic market size was estimated at USD 0.60 billion in 2025 and is projected to reach USD 2.52 billion by 2035, growing at a CAGR of 15.43% from 2026 to 2035.The Middle East & Africa held a market share of 5% in 2025. The growth of the region can be attributed to the rising global consciousness regarding ecological preservation, shifting consumer preferences towards biodegradable consumer goods, and retail packaging. The agricultural and horticultural sectors are increasingly adopting biodegradable plastic films for soil mulching, a practice that enhances crop productivity while mitigating long-term soil contamination.

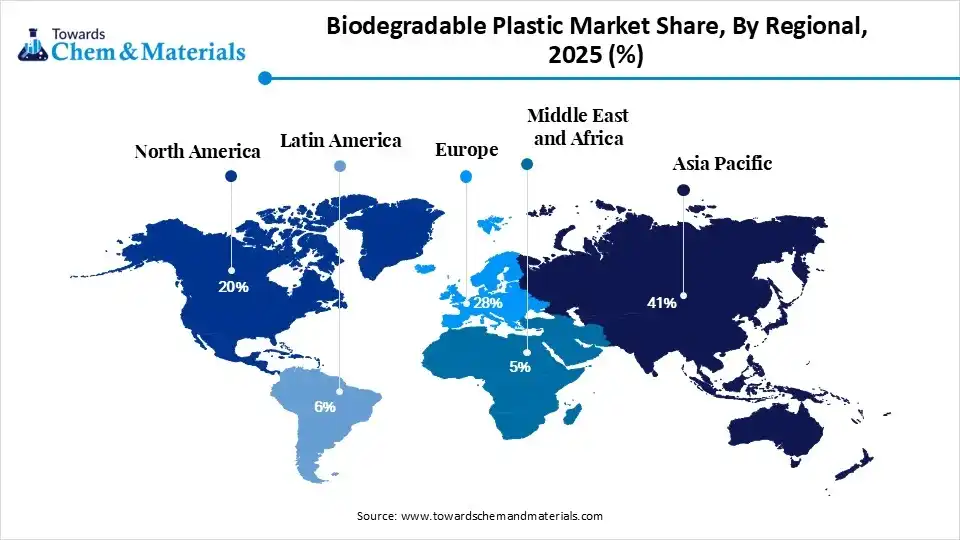

Biodegradable Plastic Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 41% |

| Europe | 28% |

| North America | 20% |

| Latin America | 6% |

| Middle East & Africa | 5% |

Saudi Arabia

- Public investments in waste sorting, composting, and waste-to-value infrastructure are drastically lowering supply-chain risks for bio-based plastics.

- Biodegradable plastics are highly sought after in the Kingdom's agricultural sector for use in mulch films, plant pots, and other items.

UAE

- Strict federal regulations banning the import, production, and trade of various single-use plastics are forcing industries to transition to sustainable alternatives.

- Advancements in polymer formulations are improving the durability and flexibility of biodegradable plastics, which help to bridge the historic price gap between bioplastics and traditional petroleum-based plastics.

Competitive Analysis

The market globally exhibits a highly competitive and fragmented landscape. Top market players are competing mainly on raw material supply security, material efficiency, and scaling production to lower costs against traditional petroleum plastics.

BASF is expanding its certified compostable ecovio® portfolio with new grades engineered to meet the evolving demands of flexible barrier packaging. This enhanced range empowers packaging manufacturers and brand owners to customize barrier performance and end-of-life solutions.

- Novamont launched a major rebrand and visual refresh for MATER-BI at the 2026 Marca trade show, reinforcing its 100% biodegradable and compostable biopolymer made from plant materials (like corn starch).(Source: www.basf.com),(Source:novamont)

Recent Developments

- In May 2026, Vary Tech, a global leader in solid waste resource utilization, announced a significant advancement in plastic recycling infrastructure. In collaboration with Evonik and SupeZET, the company has introduced a comprehensive, full-process solution designed to chemically recycle post-consumer plastic waste into high-value chemical products, including circular naphtha and plastic pyrolysis oil.(Source: worldbiomarketinsights.com)

- In January 2026, Aptar Pharma announced that its Freepod® nasal spray pump, utilized in conjunction with Haleon’s Otrivin® nasal spray, now incorporates mass-balance bio-based resins. This development represents the inaugural integration of sustainable materials into Aptar’s global drug delivery systems. His initiative marks a significant advancement in reducing the healthcare packaging industry's reliance on fossil-based plastics.(Source:worldbiomarketinsights.com)

Top Vendors in the Biodegradable Plastic Market & Their Offerings

- BASF: BASF is a premier pioneer in the biodegradable plastic market, globally recognized for its foundational PBAT polymer, ecoflex®, introduced in 1998. Their extensive biopolymer portfolio drives circular economy solutions across packaging, agriculture, and composting industries, enabling organic recycling and helping prevent microplastic accumulation in soils.

- NatureWorks LLC: NatureWorks LLC is widely recognized as a star player and dominant market leader in the global biodegradable plastics industry. The company pioneered the commercialization of bio-based polymers by leveraging massive manufacturing scale and key corporate partnerships to decouple plastic production from fossil fuels.

- TotalEnergies: TotalEnergies is a major player in the biodegradable plastics sector, primarily through TotalEnergies Corbion, a leading global producer of polylactic acid (PLA) made from renewable resources.

- Novamont S.p.A.: Novamont S.p.A. is a globally recognized pioneer and market leader in the biodegradable plastic market. Now operating as part of Versalis (Eni), the Italian-headquartered company specializes in integrating chemistry, agriculture, and environmental sustainability to manufacture fully compostable and bio-based products.

Other Key Players

- FkuR (Germany)

- DuPont (U.S.)

- Biome Bioplastics (U.K.)

- Mitsubishi Chemical Group Corporation (Japan)

- TORAY INDUSTRIES, INC. (Japan)

- Dow (U.S.)

- Plantic (Australia)

- Hubei Tianan Hongtai Biotechnology Co., Ltd. (China)

- Danimer Scientific (U.S.)

- Evonik (Germany)

- Eastman Chemical Company (U.S.)

- DAIKIN INDUSTRIES, Ltd. (Japan)

- Solvay (Belgium)

Segment Covered

By Product

- Starch-Based

- Thermoplastic Starch (TPS)

- Starch Blends

- PLA

- Packaging Grade PLA

- Fiber Grade PLA

- Injection Molding Grade PLA

- PBAT

- Flexible Film Grade PBAT

- Compostable Blend Grade PBAT

- PBS

- Bio-Based PBS

- Conventional PBS

- PHA

- PHB (Polyhydroxybutyrate)

- PHBV (Polyhydroxybutyrate-co-valerate)

- Other PHA Variants

- Others

- Cellulose-Based Plastics

- PCL (Polycaprolactone)

- Bio-Based Polymer Blends

By End Use

- Packaging

- Flexible Packaging

- Rigid Packaging

- Food Service Ware

- Compostable Bags

- Agriculture

- Mulch Films

- Plant Pots

- Controlled Release Systems

- Textiles

- Fibers

- Nonwoven Fabrics

- Consumer Goods

- Household Products

- Personal Care Products

- Disposable Consumer Products

- Others

- Medical Applications

- 3D Printing

- Electronics Applications

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (7)